A WEEK OF POSITIVE SURPRISES AND SOLID DATA

A WEEK OF POSITIVE SURPRISES AND SOLID DATA

Hello and welcome back to the No Straight Lines Investments blog, thank you so much for reading.

I am going to draw perhaps too fine a line between what constitutes a surprise and what is just plain solid economic results.

In the category of surprises this week I would include:

Chinese reduction of the RRR by 50 bps (fair to say that 25 bps was somewhat baked in)

A dovish pause by the ECB

A dovish pause by the BofC

A clean sweep of better-than-feared Manufacturing PMI’s in the US, Europe and the UK. I call this a surprise simply because all 3 were better. The magnitude of the beat in the US (which was expansionary and highest in 15 months) was most notable.

Let’s dig into all of the items above plus other key releases over the past week.

PCE - ALMOST REACHING THE PROMISED LAND

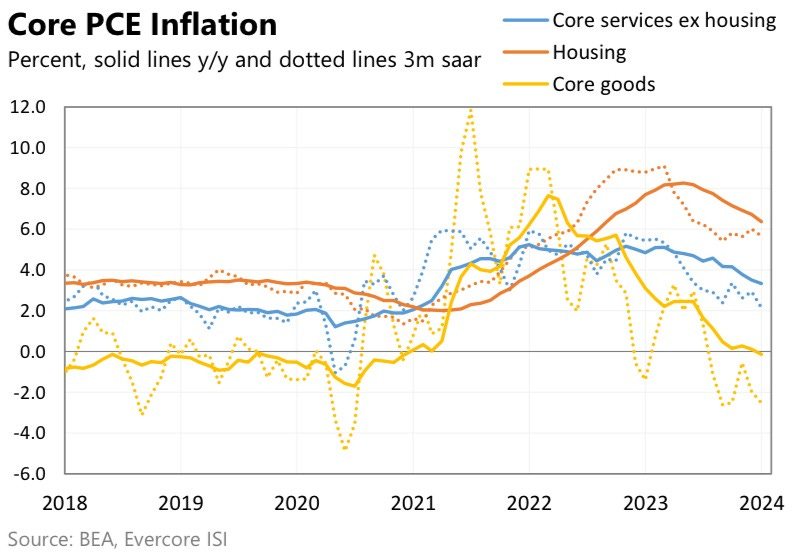

As we are all aware, PCE is the Fed’s preferred measure of inflation. Overall the data were slightly better than expected, with y/y Core PCE registering 2.9%, the first time the series has been below 3% since March of 2021. (chart from Krishna Guha, EvercoreISI)

Some commentators have suggested that 6-month core at 1.9% gives the Fed cover to cut in March.

Nick Timiraos of the WSJ thinks rate cut discussions are valid because of the following:

In June, most of the FOMC thought Core PCE would be 3.9% on a Q4/Q4 basis and projected a terminal policy rate of around 5.6%.

Instead, we ended the year at 3.2% core PCE with a 5.3% policy rate. Nick Timiraos, January 26, 2024

In a vacuum, this is very logical.

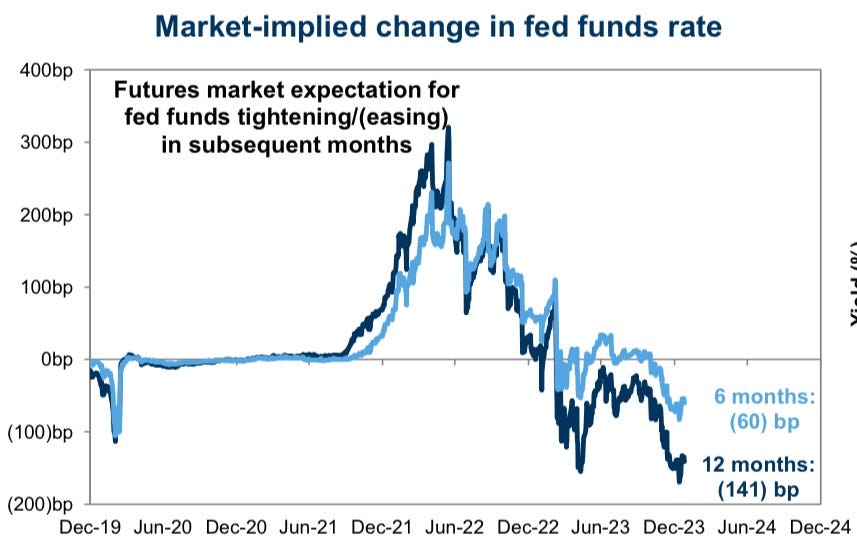

The Fed has the luxury of waiting since growth data (which we will analyze below) has been stronger than anticipated, and has led the market to remove 30 bps from easing expectations that peaked at 170 bps in December.(chart from David Kostin, GS)

I think March is still possible but it is worth highlighting that CSEH did uptick in December to 3.5% 1-month annualized, proving once again that there are No Straight Lines! (chart Krishna Guha EvercoreISI)

All kidding aside, CSEH is the Fed’s preferred measure of domestically generated inflation, according to Krishna Guha of EvercoreISI, so it is important to watch January’s read to see if the December increase was an anomaly.

One note of caution relates to the potential for goods inflation to tick back up due to Red Sea freight disruptions. It will be crucial for OER to continue lower as an offset, if this scenario plays out.

Overall, the benign PCE inflation reading certainly keeps a March rate cut on the table and is supportive of the soft landing narrative.

Q4 GDP - WHAT POTHOLE?

If we rewind a few months back, it was consensus that Q4 GDP would slow significantly (perhaps turn negative) due to student loan repayments, potential government shutdown etc.

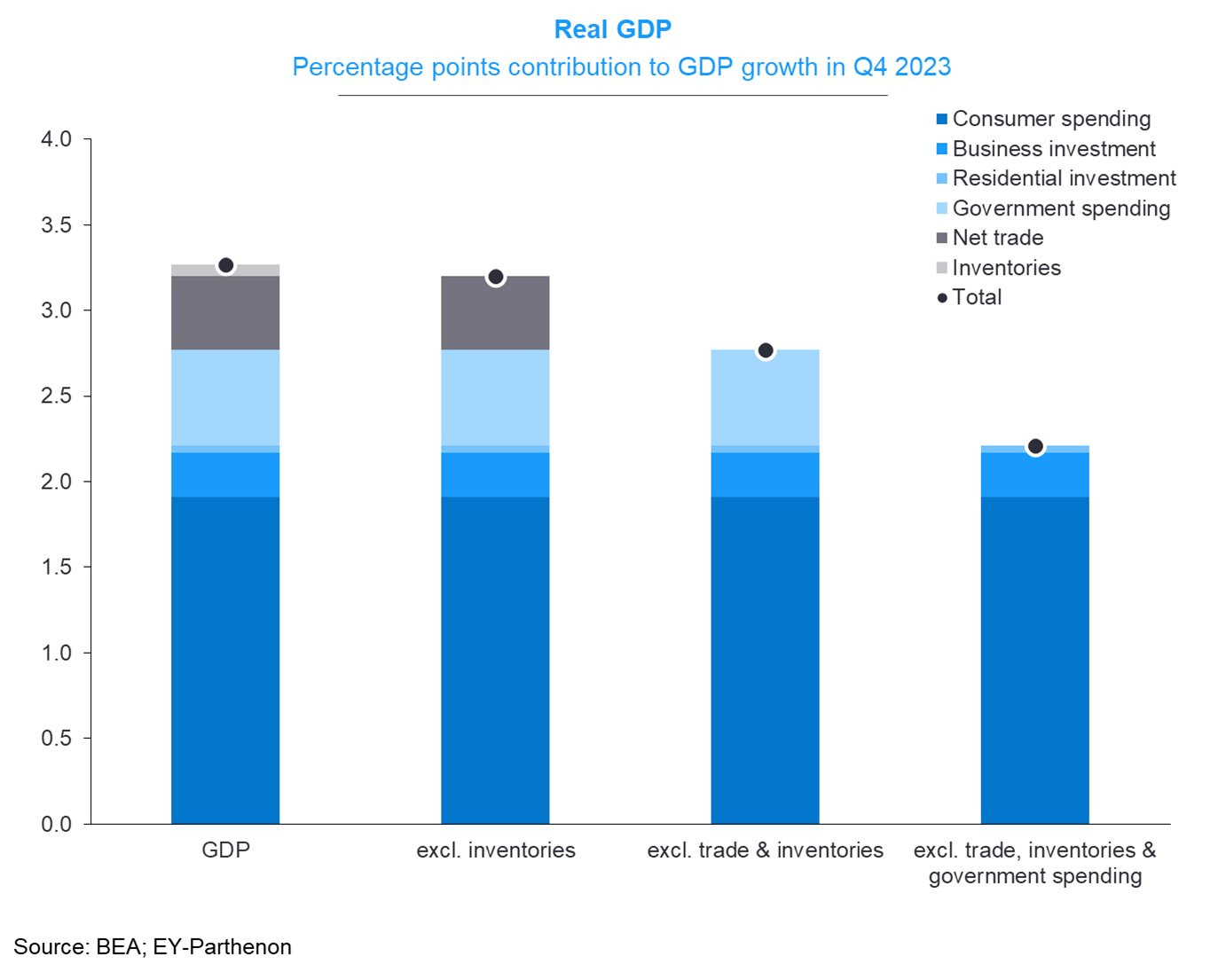

Instead Q4 GDP came in at 3.3%, against expectations of 2%, and crushing GDPNow estimates (graph from Gregory Daco).

You can see plainly that GDP accelerated in the 2H.

I really like this graph, once again from Gregory Daco, as it breaks out the categories that make up GDP

Q4 was driven by consumer spending up 2.8% q/q and representing the lion’s share of GDP.

Mr. Daco highlighted potentially the only soft spot in the remarkable performance of the US economy in 2023; namely, government spending as a proportion of GDP at 30%, was as high as it has been since 2009.

Otherwise, this was an all around solid print.

How is Q1 shaping up? Stan Shipley of EvercoreISI suggests that Q1 consumer spending is on track to be up 3%. No recession here.

Another data release strongly supporting a soft landing in the economy.

FLASH MANUFACTURING PMI’S - SIGNS OF LIFE

US

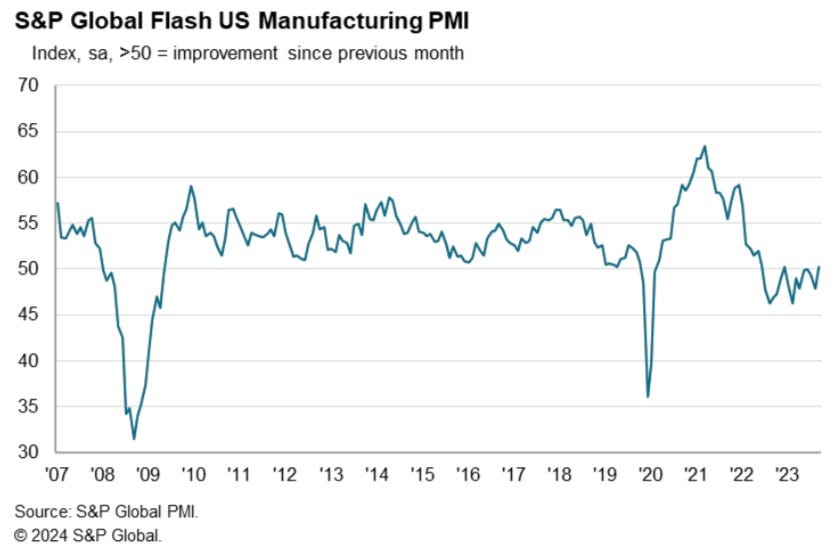

The Flash Manufacturing PMI for the US read 50.3, which means that operating conditions for goods producers improved for the first time in 9 months, and was the highest reading in 15 months.

It wasn’t all good news, as purchasing activity continued to contract, albeit at a slower rate.

Here’s the quote that caught my attention from the report:

Stocks of finished goods saw renewed expansion, indicating the fastest rise in post-production inventories since November 2022 as companies anticipate greater new orders in the coming months. S&P Global, January 24, 2024

One month doesn’t constitute a trend, but this is a very encouraging report.

EUROZONE

The Eurozone Flash Manufacturing PMI came in at 46.6, which is a 10-month high.

I would suggest the proper descriptive for the survey is “less worse”. Here are the key points:

the decline in factory production was the smallest since April of 2023

new orders decreased the least amount in the past 9 months

backlog fell less steeply than in December

optimism for the next year is at a 9 month high

This is a step in the right direction, and at a minimum is suggestive of a stabilization in the Euro manufacturing sector.

UK

UK Flash Manufacturing PMI registered 47.3, a 9-month high (noticing a trend?).

The details in the UK report were somewhat less encouraging than those in the Eurozone, particularly the fact that overall output declined at the fastest pace in 3 months.

Nevertheless, confidence for the year ahead measured the highest since May of 2023. The optimism was due to positive client signals about spending intentions, long -term business investment plans, and hopes of a broader economic turnaround.

I will be keenly watching next month’s release.

A return to growth, or at least a slowing contraction in manufacturing is a tailwind to the soft landing camp.

Moreover, a comeback in the developing market manufacturing economy is supportive for my copper and steel levered equity positions. More to come below.

PBoC ANNOUNCES 50 BPS RRR CUT

Just as global investors had given up hope on the domestic Chinese equity market, the PBoC stepped in with a larger than expected 50 bps cut to the RRR.

How do I know investors had given up hope?

First 2 graphs from Julian Emanuel of EvecoreISI.

You know it’s bad when the forward P/E on your market is less than the Price/Book of the Nas. Last graph from Mark Wilson of Goldman Sachs.

There is no question this stimulus, which will go into effect on February 5, is designed to stem the negative sentiment tide in front of Chinese New Year, which is on February 10.

As we will discuss in the flows section, the RRR cut had a dramatic impact on investor flows this week.

Even though Chinese demand for copper was better than expected in 2023, the stimulus will certainly boost sentiment toward the metal simply due to the fact that China is responsible for >50% of copper demand annually.

I will discuss in more detail later in today’s piece.

I think it’s fair to say that all commodities benefit from this announcement.

Neo Wang, China strategist for EvercoreISI expects further policy responses after the NPC meeting on March 5. Stay tuned.

THE BofC’s DOVISH PAUSE

Sometimes what you don’t say is more important than what you do say, especially when it involves Central Bank speak.

Given the outlook, Governing Council decided to hold the policy rate at 5% and continue to normalize the Bank’s balance sheet. The Council is still concerned about risks to the outlook for inflation, particularly persistence in underlying inflation. Bank of Canada, January 24, 2024

Here is the same statement from the December 6 meeting:

With further signs that monetary policy is moderating spending and relieving price pressures, Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank’s balance sheet. Governing Council is still concerned about risks to the outlook for inflation and remains prepared to raise the policy rate further if needed. Bank of Canada, December 6, 2023

By not explicitly referencing the potential to raise rates if needed, the BofC is saying that rates have peaked. That is a dovish pause folks, or even a modest pivot in my book.

In the Bank’s Monetary Policy Report released the same day, the Bank suggested that if the economy evolves as expected, the key question will be how long do they maintain rates at current levels.

The Bank is forecasting 0% GDP growth for Q1 and expects the Canadian economy to bounce back in the 2H to average 0.8% growth for all of 2024.

When will the first rate cut happen?

If the Bank’s forecast is correct (which is a big stretch since none of the Central Banks have been accurate prognosticators), it is likely an April event, which is consistent with market expectations.

This is a tailwind to equities as the focus now FULLY shifts to when the first cut will happen.

THE ECB’s DOVISH TILT

In contrast to the BofC surprise, which was in the Bank’s statement, the ECB’s Lagarde surprised markets not with the published statement but rather, with comments in post statement press conference.

Here is Krishna Guha of EvercoreISI’s take, which I think sums it up well:

Lagarde came across appreciably more dovish than the Council statement, which underlined that inflation progress has continued in spite of the anticipated bump from base effects in energy, but asserted that incoming data was broadly in-line with its expectations, rather than surprising to the downside - consistent with a stick-to-the-plan message.

We think the statement conveys that the internal consensus on the council remains June for the first rate cut.

But we take substantial signal from Lagarde that the ECB leadership - and likely a majority of the council - is not comfortable ruling out an April cut even though it is all but ruling out a March cut. Krishna Guha, January 25, 2024

The press conference repeatedly emphasized data dependence, much like the BofC and the Fed. The subtle change here is that as recently as Davos, Lagarde had suggested that the ECB needed to see 2024 annual wage data before making a decision on rates, which implied June at the earliest.

The key takeaway from the ECB and the BofC is that rate cuts are coming soon. I understand that markets had already priced cuts in, but Lagarde and Macklem have now purposefully communicated their intentions to the capital markets.

A subtle but critical change that is obviously supportive of the soft landing narrative.

This is the end of the free portion of this week’s blog. If you choose to read more (and I obviously think you should) here’s what’s in store:

A study of how equities perform when the yield curve normalizes….kinda timely I would argue?

FLOWS - where did the $$ go and what are investors doing. A big piece of the investing puzzle.

CHARTS OF THE WEEK - an efficient way to get a feel for what was moving in the market over the past week, or what may be about to move.

PORTFOLIO COMPANY WRITE UPS - this week includes my top small cap pick, which is up over 65% since I initially wrote it up last November.

If this is it, thank you so much for reading No Straight Lines Investments, I wish you the best of luck in the market this week. With FOMC and payrolls and lots of Q4 reports, it will be busy.

Until next time!