BENIGN INFLATION TREND STAYS IN MOTION

BENIGN INFLATION TREND STAYS IN MOTION

Hello and welcome back to the No Straight Lines Investments blog, thanks for checking in with me.

What an interesting week. The softer PPI print seemed to be given a bigger influence due to it’s tie-in to the Fed’s preferred PCE, but the hotter CPI print didn’t change rate cut expectations?

That is the origin of my title, which is really a play on Newton’s First law of motion: An object in motion tends to stay in motion unless an external force acts upon it.

In this case, the external force (economic data) wasn’t forceful enough!

Let’s dig into the specifics.

CPI - HOTTER BUT NOT ENOUGH TO CHANGE THE PLOTTED COURSE

I think the most important takeaway from December’s CPI numbers is that it didn’t strengthen the case for a March rate cut.

Here’s Krishna Guha of EvercoreISI’s take:

We think the Fed will not be troubled by the December CPI report, which showed monthly core CPI (up 0.31%) slightly higher than the previous month as anticipated but not as high as some had feared….The disinflation process is broadly on track for the Fed to start cutting before long. Krishna Guha, January 11, 2024

As you can see from the above graphic, shelter inflation remains stubbornly high, with housing inflation clocking in at 0.46% m/m, only slightly decelerating from November’s 0.49% m/m.

The super core measure of CSEH declined to 0.40% m/m, down from 0.44% m/m November gauge. Here’s the graphic:

The final point on the CPI data is that it MAY have marked the end of goods deflation, registering a flat month on month reading after 6 months of declines. More from PCE on that front below.

The implication is that other categories (read services) need to continue a declining trend for overall CPI to maintain it’s downward trajectory. All signs point to further declines ahead for shelter, but the realization of these lagging declines has thus far been slower than anticipated.

Remarkably, post the numbers there was no change to rate cut probabilities, as I mentioned above.

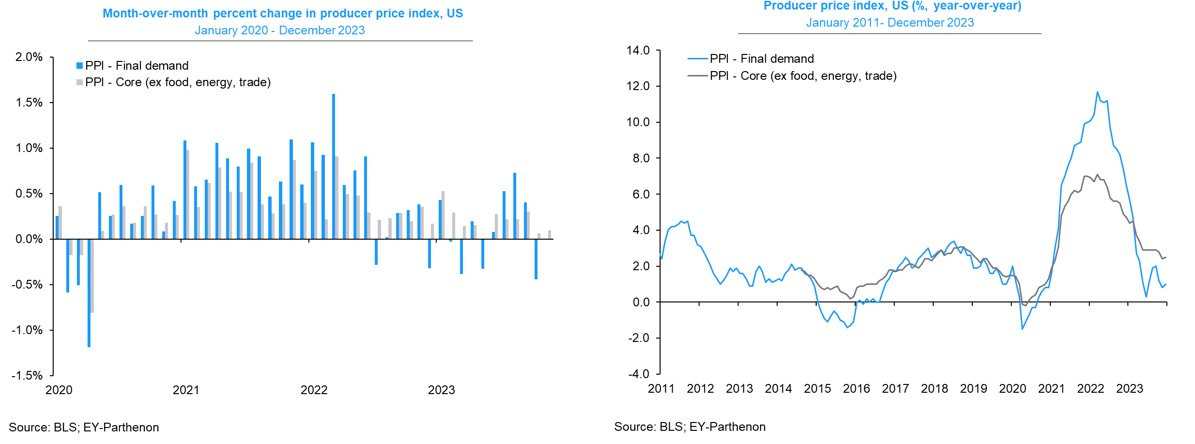

PPI - SETS TABLE FOR PCE

Given that certain components of CPI (goods deflation/hospital costs/airfares) are also part of PPI, and were elevated in CPI, the lower readings in all three categories feed into a better PCE. And PCE, we all know, is the Fed’s preferred inflation measure. Graphs from Gregory Daco.

After the CPI print, it appeared that perhaps goods deflation may have concluded. PPI wholesale goods deflation registered -0.4% m/m, which, according to Krishna Guha, suggests further goods deflation ahead.

This gives the Fed more time for service and shelter deflation to come through in the numbers.

Now that we have PPI, brokers are updating their estimates of PCE. The numbers are coming in around 0.2% m/m and PCE - CSEH at approximately 0.3% m/m.

CME Fedwatch pegs the odds of a March rate cut at 76.9% as of right now, which is up from 64% a week ago, and even nudging up from 73% after Thursday’s CPI print.

The continued downward trajectory of inflation gives the Fed cover to perhaps cut rates as early as March.

A tailwind for equities.

NY FED SURVEY INFLATION EXPECTATIONS DECLINE

If the consumer believes that inflation is going lower, they are less likely to delay purchases. The psychology is closely watched by the Fed for this reason.

As you can see in the graph from Nick Timiraos, NY Fed inflation expectations are back to where they were pre pandemic, and also match up rather well with UofMich survey results.

Also supports rate cut projections and helps the equity story.

INITIAL CLAIMS - NOTHING TO SEE HERE BUT ONGOING STRENGTH IN JOBS

Initial claims were slightly better than expected, heard that story before? It is my sincere hope that I say the same thing for many weeks to come as it would confirm that there is no recession and the soft landing has been achieved (chart from Liz Ann Sonders):

As I’ve also said previously, the chart doesn’t point to any distress in the labour market, and it was notable to me that continuing claims dropped a decent amount (34K) this week.

Let’s see if the drop in continuing claims was a blip or represents a true levelling off.

Jobs anchor the soft landing.

Story in tact, good for the equity market.

NFIB - ANOTHER GAUGE OF THE LABOUR MARKET

Immediately post the regional banking crisis in March, much attention was paid to the monthly NFIB survey, the logic being that small business would be most negatively impacted by the predicted decline in credit availability from the regional banks.

There isn’t much ink being devoted these days, but make no mistake, small business generates over 50% of new jobs, so we need to pay attention.

On that front, have a look at the latest hiring plan reading that was released last week:

I’m not sharing the graph because it shows anything remarkable.

I’m sharing it because it doesn’t show any meaningful deterioration.

That is the point folks.

For what it’s worth, the overall optimism index was up marginally this month to 91.9, but it marks 2 years of being below the 50 year average of 98.

Small business is still struggling, but things certainly don’t seem to be getting worse.

FEDSPEAK - THE RATES MARKET ISN’T BUYING WHAT GOVERNORS ARE SELLING, YET

Sometimes it can make your head spin attempting to interpret the message the Fed is attempting to convey to markets.

I wanted to share a few snippets from the past week as it is instructive of the current market backdrop.

Dallas Fed President Lorie Logan got the markets excited with a perceived suggestion about ending QT.

So given the rapid decline of the ON RRP, I think it is appropriate to consider the parameters that will guide a decision to slow the runoff of our assets. In my view, we should slow the pace of runoff as ON RRP balances approach a low level. Normalizing the balance sheet more slowly can actually help to get to a more efficient balance sheet in the long run by smoothing redistribution and reducing the likelihood that we’d have to stop prematurely. Lorie Logan, January 6, 2024

Logan, as one of the architects of QT, has sway on this subject. Her test of low balances doesn’t appear likely to be met before mid year, for what it’s worth.

A slowdown in QT is a tailwind for equities.

Governor Miki Bowman, who has been characterized by the Fed whisperer Nick Timiraos as the most hawkish member of the FOMC, had these comments:

Should inflation continue to fall closer to our 2 percent goal over time, it will eventually become appropriate to begin the process of lowering our policy rate to prevent policy from becoming overly restrictive. In my view, we are not yet at that point. Miki Bowman, January 8, 2023

Governor Bowman also suggested the possibility of another hike if incoming data requires an adjustment in Fed policy.

To me this is simply jawboning in an attempt to contain further loosening of FCI.

I will end with comments from John Williams, President and CEO of the NY Fed:

In its plans, the FOMC said that to ensure a smooth transition it intends to slow and then stop the decline in the size of the balance sheet when reserve balances are somewhat above the level it judges to be consistent with ample reserves. So far, we don’t seem to be close to that point. John Williams, January 10, 2024

As my good pal Kevin Muir (The Macro Tourist) highlighted to me, Lorie Logan was the head of the NY Fed, and Williams is the current head of the NY Fed, so the comments by Williams were seen as a modest rebuke of Logan’s suggestion that it might make sense to slow QT.

We seem to be in a market where the Fed’s comments are NOT being taken at face value. This is the condition that persisted at the outset of 2023, until it didn’t.

The difference (yes I know, dangerous to say this time is different) is that there is a clear(er) path to inflation progressing towards the Fed’s stated target of 2% now, which wasn’t the case a year ago.

A drastic change in the data would of course lead to a reassessment of future market rates.

For now, members of the FOMC are effectively pushing on a string in their efforts to rein in rate cut expectations.

It’s always entertaining to observe how Fed members attempt to say the same thing with different word choices.

Never a dull moment!

Here ends the free portion of my blog. I sincerely hope you decide to read on as I will provide:

Flow Analysis - some super interesting $$ flow and desk flow commentary which may influence your sectoral views.

Charts of the Week - a really informative and efficient manner to capture the moves in the equity market this week

Bottoms up stock/sector discussions - why I think the uranium rally is sustainable (I got long in November of 2022) and earnings results from one of my portfolio companies. The average unweighted return of stocks I have written about is over 19%.

If you are finished reading here, thanks for joining me this week, I appreciate it.

Best of luck in the week ahead.

Join my chat here on Substack for tidbits throughout the week.