BIG, BEAUTIFUL DEFICITS?

Hello and welcome back to the No Straight Lines Investments blog, I am grateful for your time and attention.

The U.S. 10-year treasury yield poked it’s head above 4.5% this week, rising 7 bps.

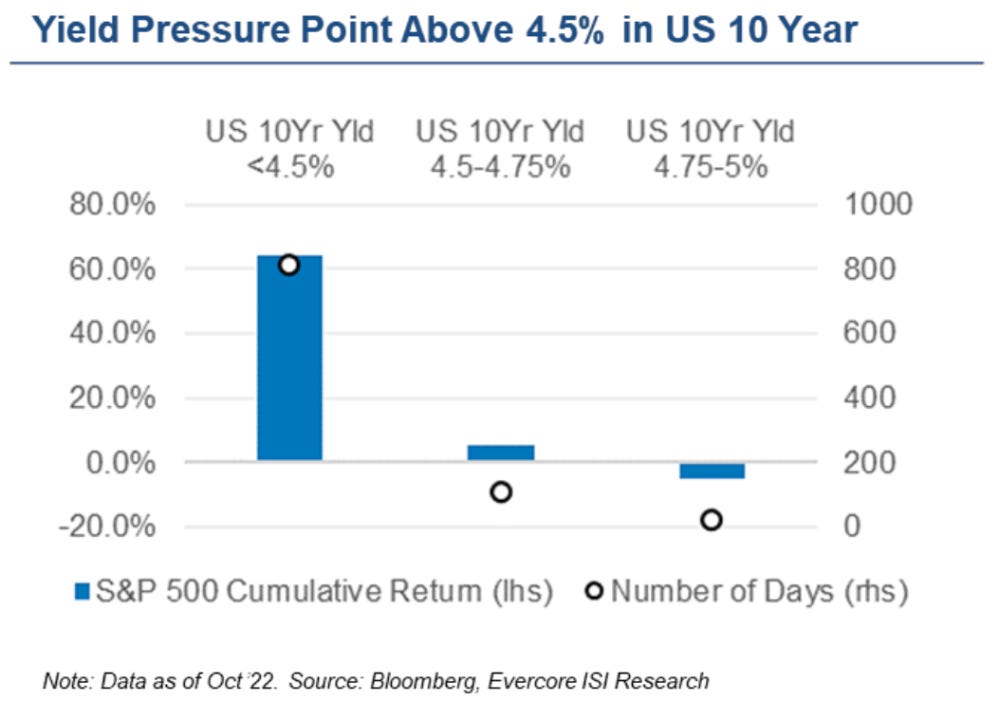

If we mark the start of the current bull market in October 2022, the chart below shows that nearly all of the S&P 500’s gains have come while the 10-year yield stayed below 4.5%—a clear signal of the pain threshold for equities.

There is little ambiguity to the yield level that inspires equity anxiety, therefore no great revelation that stocks struggled this week:

One of the (many) maddening aspects of investing is that relationships amongst variables are not stable.

For example, during the bull market of 1997-2000, the average 10-year treasury yield was 5.75%, and that clearly did not act as a headwind to equity returns.

The low in treasury yields in this time series is 4.2%.

The average yield on 10-year treasuries is 4.7% going back to 1790.

What was the root cause of the latest yield surge >4.5%?

Big, beautiful deficits to the horizon is what.

As Michael Hartnett of BofA points out, the U.S. federal budget deficit has averaged 9% of GDP over the past 5 years.

A principal aspect of the Moody’s downgrade last Friday was the fact that they foresee budget deficits continuing at that level thru to 2034.

If you wish to continue, please subscribe for $20/month:

If not (and I think you should), thanks for reading and good luck with your investments this week.

If you're hunting for bottom-up stock ideas that can actually move the needle on performance, my blog is where I dig deep—highlighting names I'm actively adding or seriously considering. That next hidden gem might already be in the mix….for the price of a couple fancy coffees. Just sayin’!

You can follow me on X (@NSLInvestments), LinkedIn: Jonathan Lansky, or use the Chat feature on the Substack app.