BIG RISK? BIG REWARD? OR BOTH? OR NEITHER?

Hello everyone and welcome to the No Straight Lines Investments blog, I really appreciate you being here!

Are you confused by the title? You should be!

I want to begin our investing journey by stating that I am about as confused as I have ever been about the stock market currently. Having said that, I should add that I don’t remember a time over the past 25+ years where there was an “all clear” to buy the stock market with abandon. These incidences are only obvious AFTER the fact. The expression hindsight is 20/20 applies perfectly to investing in stocks. It is a good practice to analyze investments we have made previously to see what we can learn from these endeavors, but lamenting missed opportunities is counterproductive.

Short story to illustrate my point?

My very first investment was the purchase of the Far East Fidelity Fund in 1987, as recommended by my father’s broker. I was 17. This particular fund was a proxy for the Japanese Nikkei index. The Nikkei index peaked in…..you guessed it, 1987!! I sold the fund in the late 90’s for less than half of the $$ I had invested. Looking back, it was OBVIOUS that I had top ticked the market, but I can tell you, when I made that purchase, I was sure I was the smartest person in the room.

Why am I so confused today?

Interest Rates and Inflation

Let’s begin here. Every Central Bank around the globe is raising interest rates in a bid to curb inflation. The desired outcome is a so-called soft landing in the economy. Rates go up enough to slow down demand and cool off price increases without causing a recession.

From my perspective the KEY challenge is that the impact of higher rates acts with a lag. As a result, the risk right now is that interest rates go up too much and cause the economy to crash. As per my comment above, only after the fact will this be blindingly apparent.

Looking back at the past 9 months of action in the market (or the past 3 days!), it is clear that as rates have risen, stocks have sold off and vice versa. As we know, there are two major reasons this happens:

Stock prices represent the sum of expected future cashflow streams, discounted back to today. So, if the discount rate (interest rate) goes up, stocks are worth less, all else equal.

Stocks compete with other asset classes (bonds/real estate etc.). If a 10-year US government bond is offering 4%, which it was briefly intraday last week, investors may choose to buy bonds over stocks. A US treasury bond is regarded as low risk, so 4% for low risk is appealing, especially considering the same piece of paper was yielding 1.51% to start the year.

The first important point I want to make is that I believe INFLATION HAS PEAKED.

There are many, many economists/analysts/commentators that are WAY smarter than I am commenting on this every day, so I am going to focus on a few specific nuggets.

SUPPLY CHAINS

Issues with global supply chains have been well documented, companies (and individuals) have struggled to obtain necessary amounts of products/parts they require to run their businesses optimally. The natural reaction to this scenario is to over order; individuals do it and so do companies. Generally, prices for the goods in demand increase, as they are scarce. However, once more product is available, what happens?

You have too much inventory as suppliers fulfill all of the excess purchase orders!! When inventories are too high, companies will cut prices until desired levels of inventory are achieved.

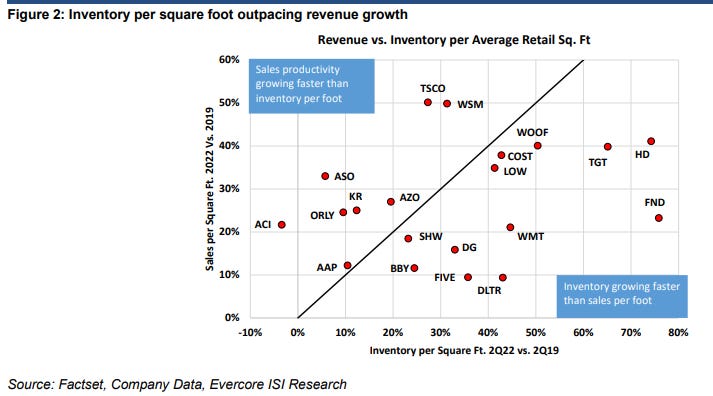

Here is a great chart from the research folks at EvercoreISI (shout out to Mr Owe!!) depicting sales growth versus inventory growth for many of the world’s largest retailers:

This scenario is playing out across a bunch of sectors, not just consumer retail. It is absolutely NOT INFLATIONARY. Inventories are bloated today which will drive prices for goods down tomorrow.

Look at the prices of commodities. Prices for oil, copper, lumber and wheat, to name a few, are significantly lower than they were 6 months ago. Again, NOT INFLATIONARY.

I also think that rate increases have slowed the economy down, especially here in Canada.

As you may be aware, the Canadian economy is extremely levered to the housing market, it represents 10% of GDP directly, approximately double that of our US neighbors. It is worth highlighting that the Bank of Canada started to hike rates aggressively before the US Fed. As a result, we are witnessing an earlier impact to our economic statistics. The bond market in Canada seems to agree as our 10-year bond yield has come down over the past 3 months.

The second major conclusion is that INTEREST RATES ARE VERY CLOSE TO PEAKING.

Why is this so crucial?

Markets are struggling because investors can’t decide at what LEVEL interest rates will peak and the length of time they will remain at peak levels. If it becomes clear on the LEVEL, at least one variable will be decided, and it will be easier for the market to find its footing.

It is well understood that the Fed is going to raise interest rates another 75 basis points at the next meeting, and another 50 basis points at the meeting that follows, so how can I argue that rates are close to peaking or may have peaked? The answer is quite simple. Markets price in expectations almost instantly these days, based on the most recent data. Just look at the price action in the US 10-year over the past few days! My belief is that the economic data is going to soften, both from an inflation and output perspective. This should create a pause in the practically parabolic rise in interest rates we have seen so far this year.

I will absolutely get the timing WRONG. Investing is not about being perfect, EVER!!

The consensus view is that rates will peak north of 4.5% in the US and slightly lower in Canada. The surprise would be rates settling HIGHER or LOWER. I am taking the UNDER.

THIS IS NOT an all clear. I AM saying that the consensus is already priced in, so you can put your money to work in businesses that can survive and thrive GIVEN the rate and inflation conditions as described above.

I am not focused on specific levels of S&P 500, the NASDAQ, NYSE or TSX. I will leave that to the technicians, for now.

I will identify specific stocks that I believe will make you and I money over the next 12 months. I have no idea what the indexes will do over the next 6 months. I predict lots of volatility because the economic data will be volatile. As I mentioned earlier, interest rate increases work with a lag. It will take time for the already announced rate hikes to do what they are intended to do!!

The reality is that making the best returns requires us to put money in the market when it feels terrible and wrong. If you stick with quality companies, it feels slightly less awful, but only slightly.

This is the perfect segue to my first stock selection.

TOPAZ ENERGY: A Software stock posing as an energy stock

This is sacrilege, how can I claim that an old-world oil and gas company is more like a new age cloud based SAAS company?

Let me explain.

We need to understand the business of Topaz first before we delve into a comparison.

Topaz is an oil and gas royalty company. They provide cash to their partners in exchange for one of the following:

A % of gas/oil production, or GORR - Topaz has GORR’s in place that provide significant leverage to burgeoning LNG Canada production (54% of acreage). If you don’t think this is a HUGE strategic advantage, think about what is currently happening in Europe and ask yourself whether the value of energy security is going to increase or decrease over the next decade. The other GORR’s cover most of the highest return energy plays in North America (specifically Clearwater). The average well on their lands pays out in less than one year. Skeptical of the oil price maintaining its current level? The highest return lands provide you with downside protection. GORR’s are 85% of Topaz revenues.

Infrastructure Ownership - Topaz takes partial ownership in gas plants/water infrastructure/CO2 capture and receives long term (minimum 10 years) commitments from the operator that guarantee a dependable income stream to Topaz. In the case of both the Glacier plant and the Weyburn potential CO2 sourcing buildout, Topaz has optionality on furthering these critical ESG positive assets. Infrastructure free cash flow covers 35% of the current dividend.

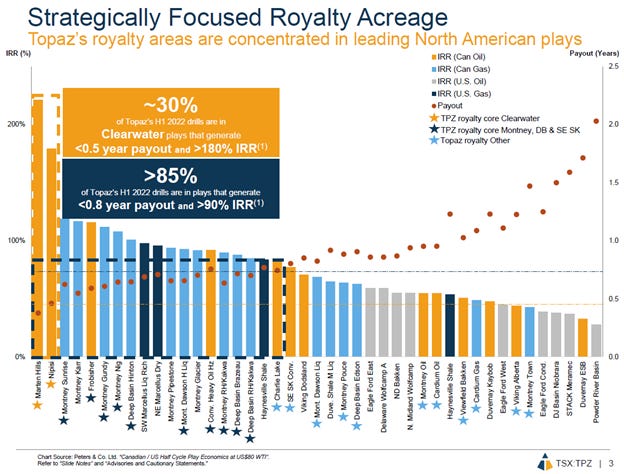

You might think Topaz sounds like a bank to its partners. The critical difference is that unlike a bank, payment is based on how the underlying asset performs. Therefore, the KEY to the success of Topaz is to make sure they only do deals involving the BEST possible assets. In terms of GORR exposure, take a look at slide 3 from the most recent Topaz corporate presentation and judge the quality of the lands for yourself:

This slide also covers off an important risk factor to Topaz. They do NOT operate any of their assets, they are dependent on their partners to spend the money. To me, the slide clearly highlights that Topaz GORR’s cover most of the highest return lands available. I believe this mitigates the likelihood of a slowdown in capital spending by their partners.

A quick point about inflation and Topaz, as it is the buzz word of the day. Topaz actually benefits from inflation. As described previously, they are not the operator, so they do not incur inflation in costs, this burden is borne by their partners. As well, they have inflation escalators in place for many of their infrastructure contracts such that Topaz receives MORE income based on specific inflation thresholds being met.

I don’t want to spend any more time describing Topaz’ business. It is a simple business to understand, just not easy to execute.

How is Topaz like a SAAS business?

Let’s discuss the attributes of the software business model that are particularly attractive to the investment crowd and understand how Topaz compares:

Scalable- Once a specific software is built i.e written and debugged; it can be sold/installed an infinite number of times without hiring a bunch more people or adding production facilities (there aren’t any). We call this operating leverage: costs increase less than revenues. This is investing nirvana.

Topaz employs 10 people to manage a business that generates $400mm of EBITDA currently. Even I can calculate that EBITDA/employee is $40mm! THAT is leverage folks. Moreover, CEO Marty Staples suggests the business could grow another 30% with the addition of only 2 more people to the current staff. Impressive stuff.

High Margin- Because software is scalable, it creates tremendous operating margins. Typical software companies generate 70% to 80% EBITDA margins. In simple terms, once the software is built, the business doesn’t require a lot of reinvestment so it generates a LOT of cash.

Topaz has a free cash flow margin of 90%+. No, that is not a typo. Every $$ of revenue comes in the door turns into $0.90 of CASH. Very few businesses, regardless of industry, generate cash like Topaz.

Annual Recurring Revenue- Investors LOVE predictable businesses and value them accordingly. Software companies with high levels of recurring revenues achieve the best market valuations. The idea is that once the software is installed, it is never removed i.e. it is RECURRING.

As discussed above, Topaz generates most of its revenue from GORR’s and infrastructure ownership. Both of these revenue streams exhibit strong predictability. Revenues are based on long term contracts which have very specific terms such as a fixed percentage of gas/oil production. Other than commodity price variability (which can be hedged), future revenues are reliably consistent. Final point here is that Topaz royalty lands have oil/gas reserves far exceeding 10 years. This provides investors with superb VISIBILITY to future revenues.

Proprietary Product- One of the key reasons that some software companies achieve lofty valuations is that they are providing a service/product that is unique and creates value to the organizations who deploy it. Hence the software installation is STICKY.

Topaz is a unique source of financing for energy companies, full stop. In today’s world, it is very difficult for an energy company to attract financing. The investing crowd is rightly concerned about climate change and views energy companies as leading contributors to our worsening climate. This is a topic for another post. Topaz CAN provide financing to energy companies in a win-win scenario: Topaz adds another royalty to its growing list of high quality GORR’s, and the energy company gets much needed capital at a lower cost than straight equity or debt.

Topaz is able to be VERY selective about which deals they execute as a consequence of their unique position in the capital stack. The pipeline of potential deals is bigger than it has ever been. The end result is an incredibly high quality, dependable and GROWING base of royalty and infrastructure revenues. To wit, the company currently has 13% of the drilling rigs in Western Canada deployed on its royalty lands.

Growth- Due to the proprietary nature of the product, there is typically a long runway of visible growth for high multiple SAAS businesses. If you provide a solution that makes businesses more efficient and profitable, companies will be knocking on your door to install the product.

Based on its unique position in the capital stack of potential partners (not debt and not equity), hopefully it’s obvious that Topaz has a huge funnel of potential new deals available. Notwithstanding this backdrop, even if Topaz never signed another deal, the company could grow its business by 5% to 8%/year for the next 5 years, simply based on the capital plans of its partners. Given the enormous free cash flow generated by the business, I am going to suggest that with annual acquisitions, the company could grow 10%/year without ever issuing equity.

Why does ANY of this matter?

It all has to do with how Topaz is valued by the investment community.

A typical large cap SAAS company is currently trading at 24x 2023 EBITDA estimates, assuming 14% y/y growth and 21% free cash flow margin.

Shout out to my friend Richie B for the above stats!

I understand that many, if not all of you will be dismissive of the comparison simply because Topaz is an oil and gas company. Imagine if we were doing a blind tasting of a beverage, and SAAS businesses were in one brown bag and Topaz was in another. I honestly believe they would taste pretty much the same. That being said, Topaz currently trades at 9x 2022 EBITDA, quite a substantial discount!

In my view, Topaz screens exceptionally well on scalability, profitability, proprietary offering and predictability. On growth, SAAS businesses get the nod. The offset from a Topaz investor perspective is twofold:

Dividend: The company currently pays $1.20/share in dividends, which equates to a 5.5% yield at today’s closing price of $21.97. This dividend will grow as the business grows. High growth SAAS businesses do not typically pay dividends as the investment community wants excess cashflow reinvested in the business to maximize growth!!

Risk of obsolescence: Many of you will disagree with me, but I am going to state that demand for oil and gas, and more specifically, NORTH AMERICAN oil and gas, will remain strong for a very long time. The energy crisis in Europe illustrates why I feel such conviction. By definition, software is a product that is constantly being improved, so there IS a legitimate risk of demand diminishing, margins coming down, or both.

On balance, Topaz should trade closer to a SAAS multiple than not. If we provide some discount based on the lower growth profile, even 15x ebitda seems justifiable.

All else being equal, over the next 12 months, the stock could appreciate 50% based on multiple expansion. If multiple expansion is not in the cards, growth in the base business will support 10% appreciation + dividend, which is a tidy 15% + return from today’s price.

FUN STUFF

I don’t want the blog to be ALL about stocks. Each post I will try to come up with a question or an observation or whatever for our community to think about and comment, if interested.

For this week, I would like to know: WHAT IS YOUR FAVOURITE BUSINESS BOOK?

My pick is Shoe Dog by Phil Knight.

It is an autobiography for certain. However, there are a million lessons about business and life in this gem. I highly recommend!

Until next time, good luck in the market!

Please share this post with anyone you think would find it interesting or useful.

Thanks in advance,

Jonathan

Just found you via another blog, looking forward to reading from the start.

I own some of the companies you mention, so looking forward to your thoughts.

Thanks for what you're doing.

Great first piece JL ! Can't wait for more !