DEJA VU ALL OVER AGAIN

A warm welcome back to the No Straight Lines Investments blog. I am grateful to you for joining me here as I try to puzzle my way through yet another intriguing week of action in the equity market.

We finally broke through and reached an ATH in the S&P 500 and Nasdaq, driven mostly by resurgence in AI leaders (think NVDA/META/AMD/TSM). I will discuss this in more detail below.

So the performance of the S&P was fueled by AI enthusiasm, doesn’t this sound familiar??

In a week where the 10-year US treasury backed up 20 bps to 4.15%, the S&P 500 advanced 1.5% and the NDX roared ahead by 2.9%.

In keeping with the pattern over most of 2023, the Russell 2k was down 0.3% and is down over 4% to start calendar 2024.

Will be interesting if the breakdown of the correlation between rates and equities continues this week, at least with regards to the NDX and the SPX.

We will now dive into the “why” behind the backup in rates, as we know all rate increases are not treated equally by equities.

WALLER PACKS A WALLOP

When the time is right to begin lowering rates, I believe it can and should be lowered methodically and carefully. In many previous cycles, which began after shocks to the economy either threatened or caused a recession, the FOMC cut rates reactively and did so quickly and often by large amounts. This cycle, however, with economic activity and labour markets in good shape and inflation coming down gradually to 2 percent, I see no reason to move as quickly or cut as rapidly as in the past. Christopher Waller, January 16, 2024

Remember I wrote last week that Fed speakers were effectively pushing on a string to keep rate cut expectations in check?

Seems Governor Waller carries some sway and the bond market stood up and paid attention.

Goldman’s Jan Hatzius didn’t back away from his prediction of a 25 bps cut in March, but he DID acknowledge that Waller’s comments increased the risk of of the first cut happening later.

There were 2 other points worth repeating in Waller’s speech:

FCI - much ink has been spilled (including by yours truly) about the historic loosening in financial conditions since yields peaked in October last year. Waller’s view is the conditions are roughly as tight as they were in July, at the time of the FOMC’s last hike, and he views that level as appropriate and able to continue to slow the economy. VERY interesting.

Labour Market Commentary - Waller highlighted a paper he had co-written which argued that restrictive monetary policy could lower the job vacancy rate from 7.5% to 4.5% without a significant increase in the unemployment rate, which is exactly how things have played out.

The key takeaway is that the vacancy rate is at 5.3% now, and Waller suggested that the FOMC is wary of over tightening now that the rate is closer to the 4.5% threshold identified in his paper of 2 years ago.

The 10-year was up 12 bps after the Waller speech. Enough said.

DEMISE OF THE US CONSUMER GREATLY EXAGGERATED

We are all well aware of the crucial role the consumer plays in the US economy, it’s the reason retail sales are closely watched.

Retail sales came in better than expected at 0.6% m/m.

Most significantly, with December in the books, EvercoreISI is forecasting real consumer spending to be up 2.3% in Q4.

Post the release of the retail sales figures and the IP/Manufacturing data (see below), GDPNow estimates for Q4 ticked up to 2.4%.

If Q4 is truly a speed bump, perhaps we need to consider the “No Landing” scenario.

I’m not going there yet, but the strength of the consumer certainly augers well for a soft landing.

This is a prime example of better economic data leading to a back up in rates. It isn’t bad news!

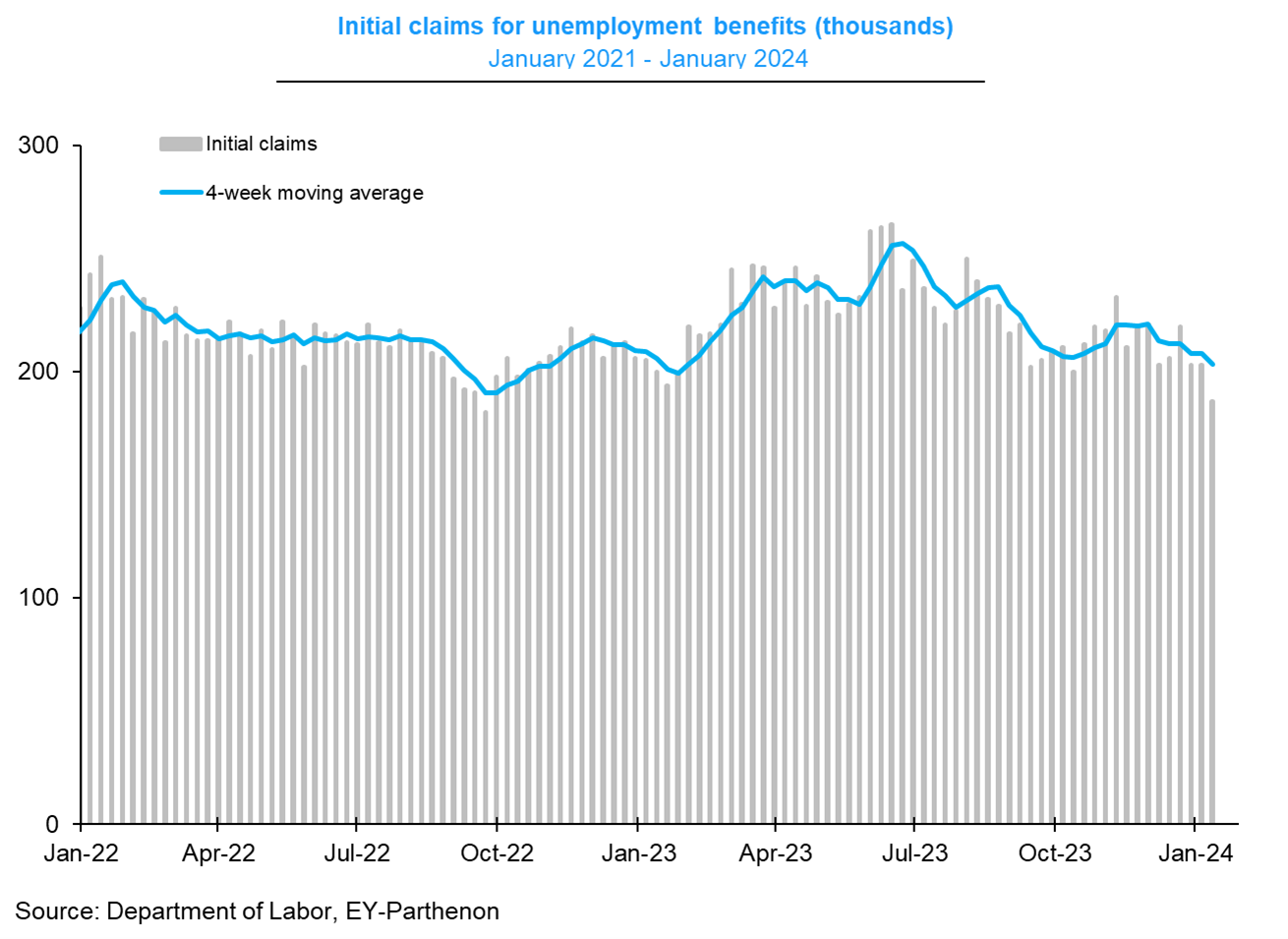

INITIAL CLAIMS REMAIN VERY LOW

Initial claims clocked in well below expectations at 187k. I would note that there may be some “noise” in the results this week due to the extreme cold in most of the US.

Graph from Gregory Daco.

We only have one more claims release before January payrolls are released.

For Q4, payrolls averaged 165k/month. Current consensus is clustering around 175k adds, which is almost double the amount required to keep unemployment flat, all else being equal.

Job creation continues to be supportive of the soft landing scenario, and a tailwind for equities.

UofMICHIGAN YEAR AHEAD INFLATION EXPECTATIONS

Much like the NY Fed survey results from a few weeks ago, year ahead inflation expectations declined 0.2% to 2.9%, the lowest reading since December of 2020.

I would be remiss not to mention that overall sentiment rose to 78.8, which was the highest since July of 2021, and a sharp acceleration from November’s 69.7 reading.

The forward inflation reading bolsters the rate cut case and overall helpful to equities.

Graph from Gregory Daco.

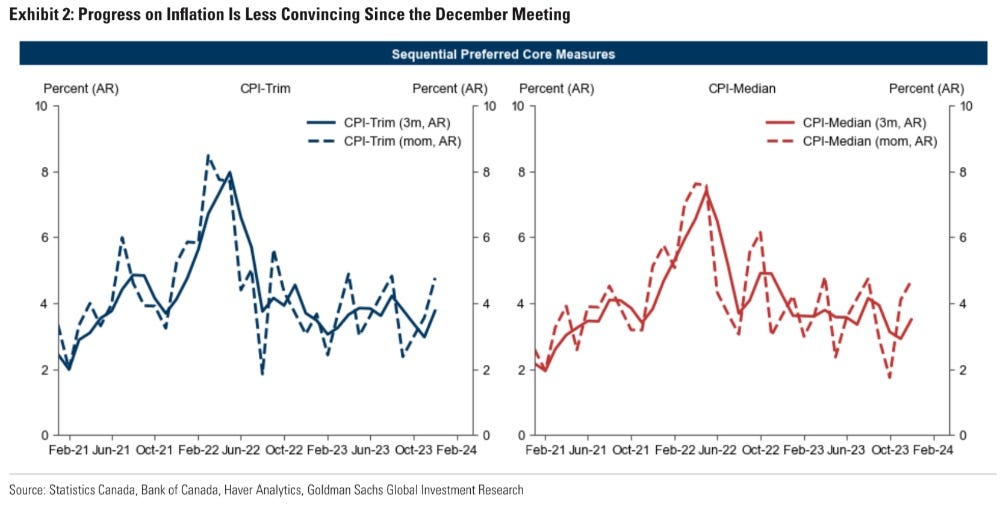

CANADA CPI SLIGHTLY HOTTER

As you can see from the graph, headline CPI ticked up 0.3% to 3.4%, which was in-line with consensus.

The slightly troubling aspect of the release was the uptick in the BofC’s preferred measures, shown in the graphs, courtesy of Goldman Sachs:

CPI-trim accelerated to 3.8% against 3.2% last.

CPI-mean was up to 3.5% versus 2.8% last.

Digging into the details, once again Mortgage Interest was the largest contributor to inflation (up 28.6% y/y). Excluding this item, inflation would have been 2.5%.

Douglas Porter of BMO shared a super interesting (to me) tidbit, that for all of 2023 Canadian headline inflation averaged 3.9%, whilst the comparable number for the US is 4.1%.

If I was forced to guess, I would have picked Canada to have higher inflation over the past 12 months.

It’s interesting that both Canadian and US CPI was slightly hotter for December.

I don’t think it changes the calculus for the BofC, I still expect a rate cut by April.

The most recent CPI is a clear indication that the downward descent of inflation will not be perfectly smooth. Goldman has pushed out rate cut expectations to June, but still expects 100 bps of cuts in 2024.

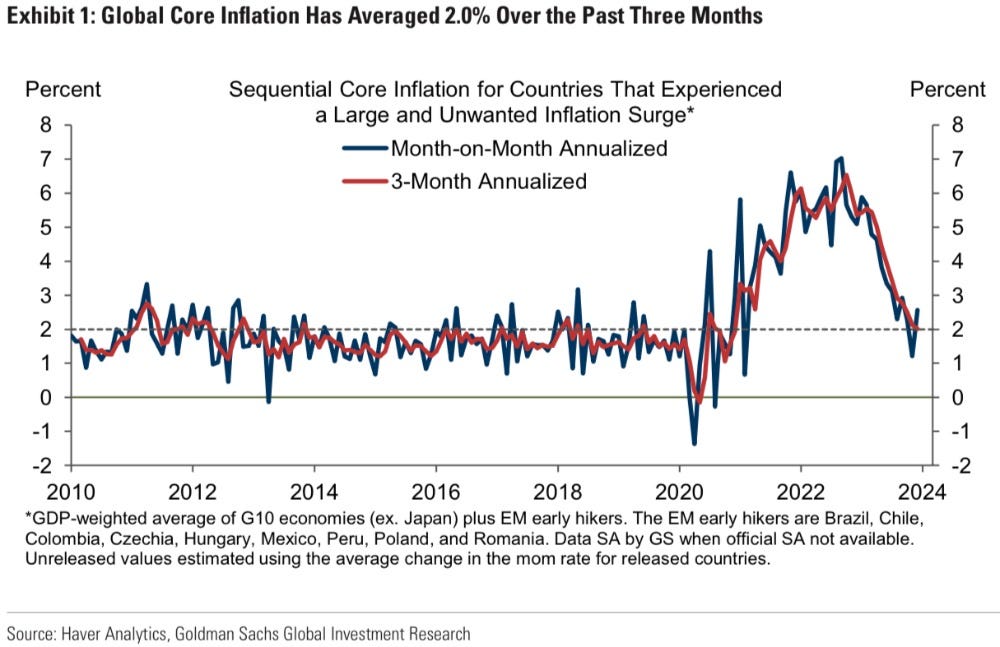

For some global context, check out this graph from Goldman’s Jan Hatzius:

As you can see, 1-month annualized inflation ticked up to 2.6% from 1.2% in November.

I would note this calculation was done prior to the upside surprise in UK inflation.

Hatzius and team remain convinced this is not a harbinger of more inflation increases to come for three main reasons:

3-month annualized inflation is still on a downtrend, at 2% for December.

Core goods inflation has further to fall. Last week’s PPI certainly supports this assertion.

They continue to forecast that services and wage inflation will gradually decline as a result of better balance in supply and demand (echoed in Governor Waller’s comments above).

Given how right Mr. Hatzius has been over the past 1.5 yrs, I am leaning into his predictions.

A Few Other Tidbits

Empire Manufacturing/Philly Fed - the results of the Empire were so bad (same level as during peak of COVID, when everything was shut down) that they are likely a “fluke” in the words of Ed Hyman of EvercoreISI. Philly Fed was better than expected, so I’ll call this series a wash.

IP/Manufacturing - overall anemic growth but I would suggest the numbers are better than the awful Manufacturing PMI readings over the past year +. I am watching closely for signs of recovery as copper and steel will obviously be strongly influenced by these readings. Have a look at the graph by Gregory Daco.

Housing Starts - came in better than expected at 1.46mm, although meaningfully decelerating from November’s blistering pace. The reason we need to pay attention is because every 100k increase in starts, adds about 0.4% to annual GDP, according to Stan Shipley of EvercoreISI. With mortgage rates dropping, signs are pointing to better days ahead in the housing market, look no further than the public homebuilders.

So where did we end up with respect to rate cut expectations after a week of mostly stronger economic data? According to CME Fedwatch, there is a 48.1% probability of a rate cut in March, which is down rather dramatically from 76.9% a week ago.

Higher expected rates from an improved economic outlook is a much better outcome than higher rates due to persistent inflation.

This is the end of the free portion of this week’s blog. I genuinely hope you continue to read as I will delve into:

Weekly Flows and Trading Colour - a key part of understanding market behaviour is keeping close tabs on $$ flows and investor activity at the brokers. This is particularly true with all of the cross currents of news in today’s market environment. Talk is cheap, follow the $$.

Charts of the Week - examining notable charts from this past week, a quick way to see where the action was and get a feel for the sectors that investors are both investing in and avoiding.

Bottoms Up Analysis - one of my core positions reported earlier this week, I will dig into the numbers and conference call thoughts. I believe the stock is a key beneficiary of lower rates in 2024.

Thanks for reading No Straight Lines Investments blog, I wish you the best of luck with your investments this week!