FED HEADFAKE FAILS TO DERAIL THE MARKET

FED HEADFAKE FAILS TO DERAIL THE MARKET

Hello and welcome back to another edition of the No Straight Lines Investments blog, thanks for joining me.

You could be forgiven if you experienced a bit of whiplash in this week’s action.

I wanted to start with this chart because I think the average market observer (I am including myself in this cohort) would likely be surprised that the 10-year US treasury yield closed down 13 bps on the week.

Considering the pushback from Chairman Powell against a March cut and the blowout January payrolls report, it is quite telling that yields were lower overall on the week, don’t you agree?

Stepping back, it remains clear that growth is holding up better (accelerating?) than expected and inflation is moving lower, albeit with some bumps (AHE latest example) along the way.

Let’s dive in!

FOMC - STATEMENT MORE DOVISH THAN PRESSER

In a pattern that has been highlighted by the savvy Mohamed El-Erian, between the release of the prepared statement accompanying the rate decision of the FOMC, which leaned dovish, and the press conference, where JPow was decidedly more hawkish, the markets were quite volatile.

A great summary from Krishna Guha of EvercoreISI:

But the Fed is not going to cut in March absent a labour market scare - which has been our basic read all along (non-discretionary bad news path=March, discretionary good news path = May or June).

The Fed Chair’s unequivocal message was jarring after the revised FOMC statement leaned clearly May/June not March but kept all options open, including the possibility that sufficient evidence might arrive on an accelerated March timeline, though it was likely to take longer.

The market sold off sharply on Powell’s not-March statement, possibly more than was warranted.

The Fed’s message remains very constructive. Growth is strong, employment is strong and inflation is already down to 2% on a high frequency basis. Krishna Guha, January 31, 2024.

JPow’s pushback against a March cut looks particularly prescient given the strength of the January payrolls, but the FOMC was not in possession of this data point on Wednesday.

Much time was spent in the press conference deciphering what the FOMC would regard as “sustainable progress toward 2%”.

JPow suggested that goods inflation would likely normalize and the FOMC would like to see further evidence of services deflation, specifically OER.

On this point, Krishna Guha provided 2 helpful calculations:

Current 6-month annualized core PCE with goods inflation at zero = 2.5%

Same calculation adjusted for “normalized OER” and core goods at zero = 2.2%

There are many measures of rent that indicate further declines in OER are forthcoming, so it isn’t a stretch to suggest that the above calculations are within reach, more a question of WHEN.

The key takeaway from all of this is that the street didn’t change the number of cuts forecast for 2024 (5), but the timing of the first cut is simply postponed until May instead of March.

In spite of the 1.5%+ drawdown in equities post FOMC, the market finished up on the week, which is broadly bullish.

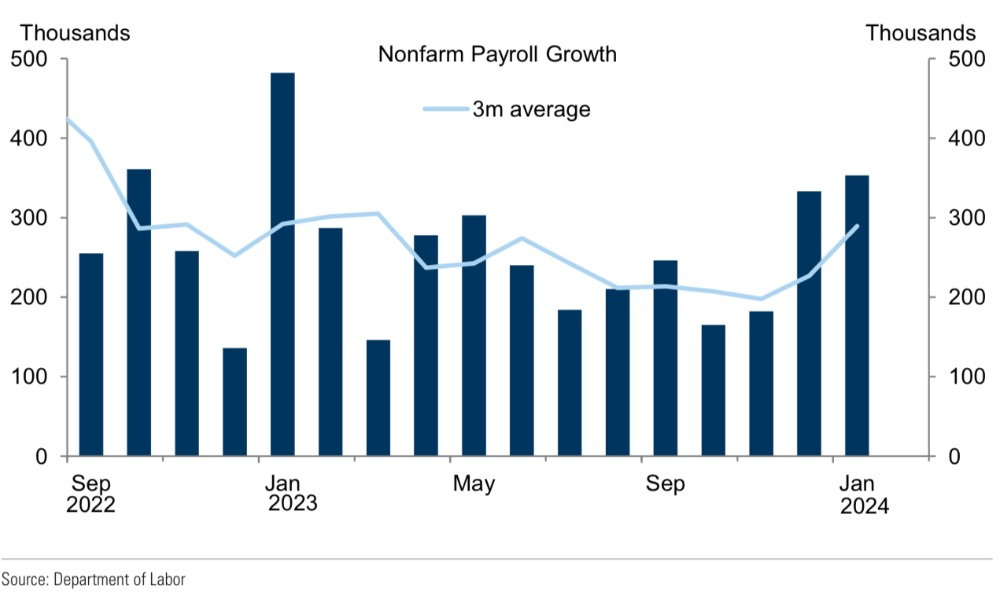

PAYROLLS - HARD TO POKE HOLES IN STELLAR JANUARY REPORT

Payrolls advanced 168k above consensus, registering at 353k new jobs.

A lot has been made of the negative revisions to previous months results. The January report actually made an average positive revision of 62k to the previous 3 months survey data. (graph from Jan Hatzius GS)

Perhaps the most encouraging aspect of a decidedly positive report was the breadth of job gains. There has been an outsized portion of gains attributed to: Education/Healthcare/Leisure & Hospitality/Government. In January, these sectors counted for 45% of jobs created, down from 82% and 53% in November and December respectively. (graph from Krishna Guha, EvercoreISI).

Wages were hotter than expected at 0.6% m/m, pushing up the 12 month figure to 4.5%.

As pointed out by Jan Hatzius of Goldman Sachs, some of this is likely due to the shorter workweek, and some of it could be due to the severe weather in January.

ECI & Productivity

Whatever the case may be, it does contrast rather starkly with the benign Q4 ECI reading released on Wednesday, which came in slightly below expectations at 0.9%, and was the lowest reading since Q2 of 2021.

The level of ECI currently is more consistent with 2% inflation.

Another welcome data point were the Q4 productivity numbers, which came in at 3.2% q/q. Q4 to Q4 annualized, the number is 2.7%, which is historically high(graph from Gregory Daco).

Why should you care about productivity?

It keeps a lid on inflation whilst allowing the economy to grow, that’s why!

It is one of the concerns about the Canadian economy, considering we have similar levels of wage inflation.

Without question, maintaining a healthy jobs market is the key component of the soft landing.

January’s payroll numbers emphatically reinforce that the economy is strong and augers well for continued strength in the US consumer.

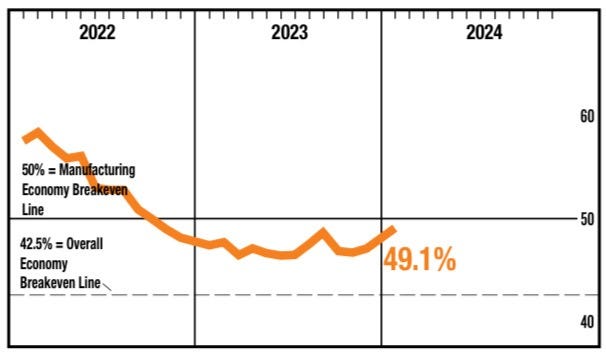

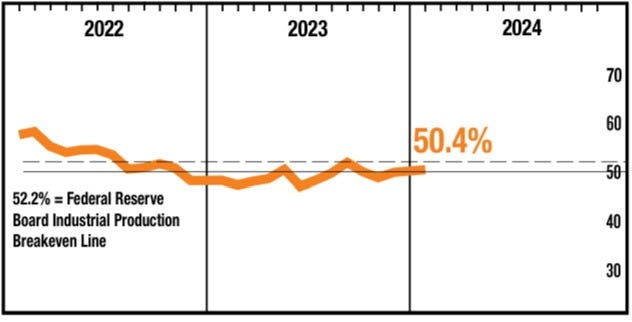

MANUFACTURING PMI

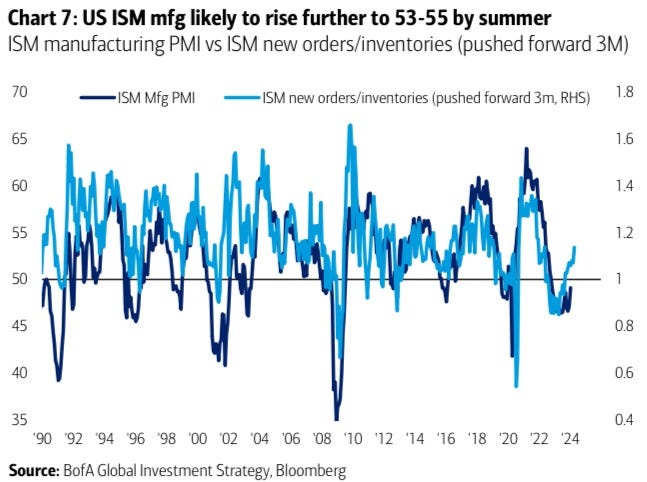

The ISM Manufacturing PMI came in at 49.1, which is the highest result since October of 2022. Just as significantly, in my mind anyway, was that the final reading of the S&P Manufacturing PMI registered 50.7. (first 3 graphs from ISM)

New orders expanded for only the 2nd time in 20 months. As you can see from the graph, there was zero expansion for all of 2023.

Production also expanded in January, albeit less so than New Orders.

We need to see a continuation of these survey results for the next few months, but it certainly appears that the manufacturing economy is on the upswing.

I sure hope Michael Hartnett is correct about orders leading the ISM.

A manufacturing recovery is a key component of my copper and steel thesis, so these releases were welcome news.

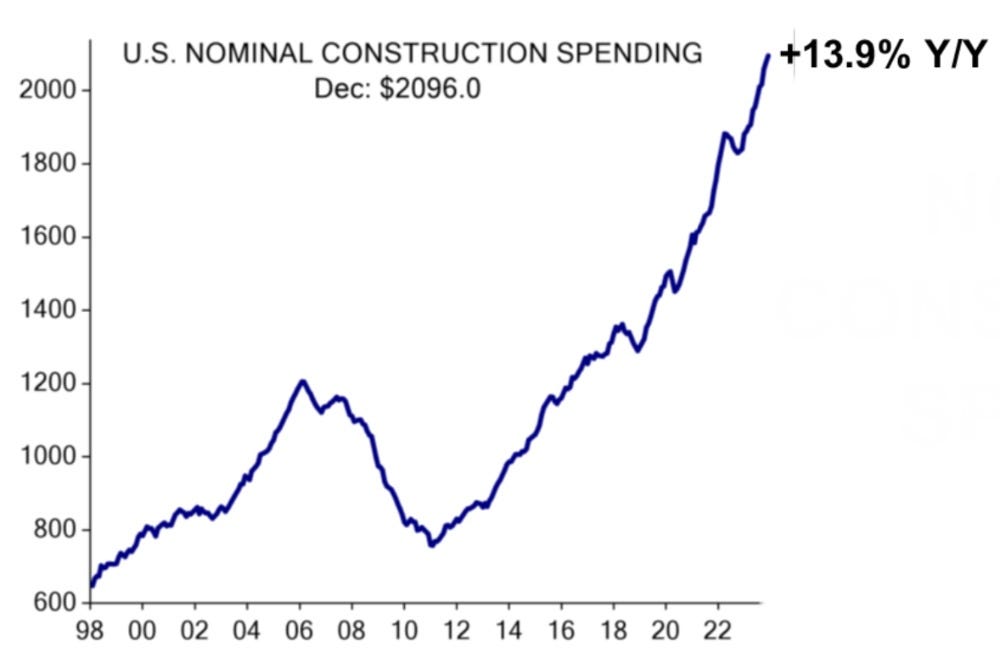

I would be remiss not to mention the 0.9% jump in construction spending for January, which obviously supports the steel/copper case as well. (graph from Ed Hyman EvercoreISI)

CANADA GDP - BETTER THAN FEARED

It would appear that rumours of the Canadian economy’s demise have been exaggerated.

November numbers of 0.2% and December’s flash estimate of 0.3% were both ahead of expectations.

In fact, if the flash number ends up being accurate (it is prone to revisions), it suggests that the Canadian economy exited the year growing north of 2% Q4 annualized.

For perspective, the recently released BofC MPR had forecast 0% growth for Q4. That’s a rather large delta isn’t it?

BMO’s Douglas Porter had this to say about the numbers:

Notably, most of the growth in November (and apparently in December too) came from the goods producing sectors, and particularly manufacturing and resources. Since these sectors are heavily influenced by exports, it seems that the surprising resiliency in the US economy is indeed spilling over into some sectors in Canada. Douglas Porter, BMO, January 31, 2024

Canada’s economy is inextricably linked to the US, it is obviously known, but I don’t think it is well appreciated by investors.

Porter suggests there is upside risk to his 2024 GDP estimate of 0.5% given the ongoing strength in the US numbers.

The key takeaway is a likely push out for a March cut from the BofC.

At the very least, it gives the BofC the option of cutting from a position of strength, rather than in reaction to weaker economic numbers.

As with the FOMC, the BofC will see plenty of data before it’s next decision.

Certainly the GDP numbers are a support for a Canadian soft landing.

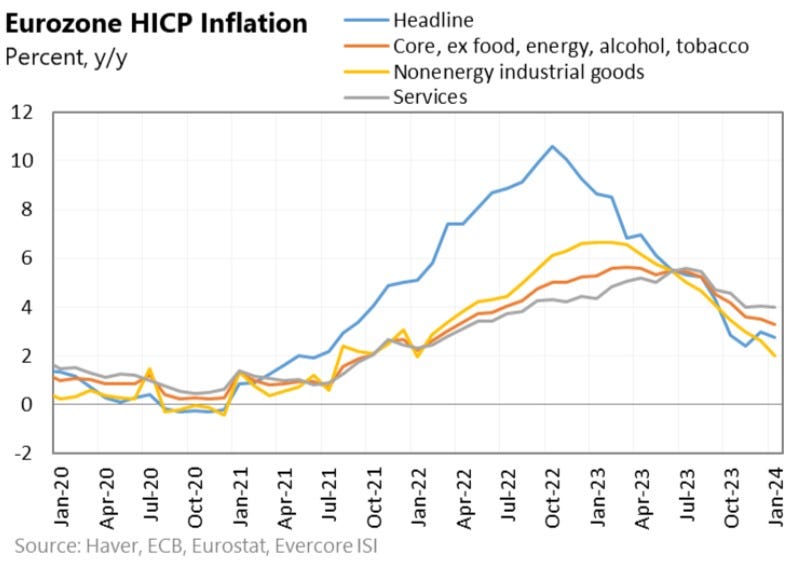

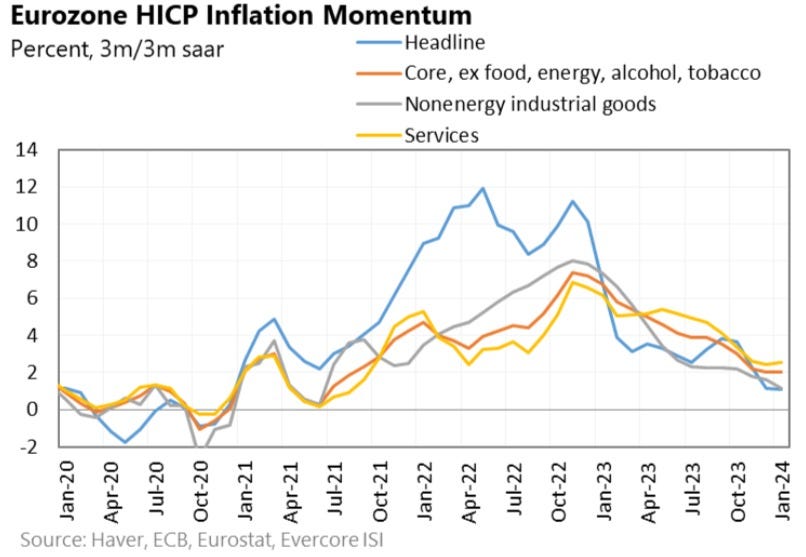

EZ INFLATION

Both headline and core CPI for the Eurozone came in slightly above expectations at 3.3% and 2.8% respectively.

Services inflation remained stubbornly high at 4% for the third month running. Does this sound familiar to anyone?

Given that Lagarde had specifically identified services as an area of concern, naturally one could conclude that expectations for an April cut might be in jeopardy.

Coupled with the better than expected EZ GDP performance, it might mean that the ECB feels more inclined to wait and see based on incoming data. (graphs from Krishna Guha EvercoreISI)

You can see that there is still a solid downtrend in place, but the trip will not necessarily be a smooth one.

GDP NOW

As of February 1st, the Atlanta Fed GDP now is 4.2% for Q1. Wow!

This does NOT include the January payrolls data, which is going to lead to a positive revision. It does include the ISM PMI and construction spending releases, which were both stronger than expected.

We are barely a month into Q1 so lots of time for negative (and positive) revisions, but this is a good start and supportive of the “no recession” arguement.

TREASURY FUNDING/TREASURY AUCTION

If you recall, back in September when yields began their move to 5% on the 10-year, one of the driving forces was the giant supply of US treasuries that were anticipated to be coming to market.

Fast forward to this week, and there were 2 benign data points which contributed to yields finishing the week lower:

Treasury Funding - at $760B, it was $55B lower than the previous estimate, which came out in October. Check.

Treasury Auctions - at $121B, was bang in-line with expectations. There were heightened concerns around this announcement, hence the rally in bonds post release

As you folks are well aware, I am an equity person, but this was a crucial release that had a material impact on the bond market.

This is the end of the free portion of my blog, if you decide to continue here’s what’s in store:

Q4 Earnings Commentary - earnings scorecard so far, and a particular emphasis on the Mag 7 and why they are so crucial to having an informed view on the markets

Flows - in depth look at where the $$ are being allocated, both from a MF/ETF perspective and also on the trading desks. Talk is cheap, follow the $$.

Charts of the Week - this week features charts from several sectors, not just tech, you might just discover your next great idea.

My Portfolio - I dive into some factors that I believe bode well for one of my key themes as well as updating my views on another core name in light of a recent upgrade from one of the big brokers.

If this is it for you, thanks again for reading.

I wish you the best of luck with your investments this week.

You can follow me on X: @NSLInvestments

I also use the chat function on the Substack app throughout the week and I post to LinkedIn.

If you have feedback or questions please reach out, I would love to hear from you.

All the best.