GROWTH INSPIRED RATE CREEP IS GOOD FOR EQUITIES

GROWTH INSPIRED RATE CREEP IS GOOD FOR EQUITIES

Hello and thanks for checking in to read this week’s edition of No Straight Lines Investments. It was a data light week but still lots of fascinating action to decipher.

Due to a combination of moderate FOMC pushback but mostly due to stronger overall data (ISM Services being the standout this week), we have seen the odds of a March rate cut fall from 85% coming into 2024 to 16% currently.

There has been a corresponding rise in the 10-year US treasury yield of just under 30 bps to 4.17%.

And yet equity indices are solidly positive YTD:

SPX +5.4%

NDX +6.8%

TSX +0.24% (yeah I know I am reaching a bit….)

Whilst the IWM (Russell 2k) is modestly negative on the year (thank you regional banks), it was up 2.4% this week, solidly beating SPX (+1.4%) and NDX (+1.8%), a welcome broadening out of performance.

Stocks are doing well because the economy is doing well. The combination of solid growth with benign inflation is a supportive equity backdrop. Period.

Let’s dig in.

ISM SERVICES - ANOTHER ARROW IN THE QUIVER OF STRONG ECONOMY

With 2/3 of the US economy tied to services, continued strength in the ISM reading suggests that GDP growth will remain solid for Q1.

In fact, January’s reading of 53.4 is consistent with 1.5% annualized real GDP growth (according to ISM).

The current GDPNow estimate is 3.4% for Q1.

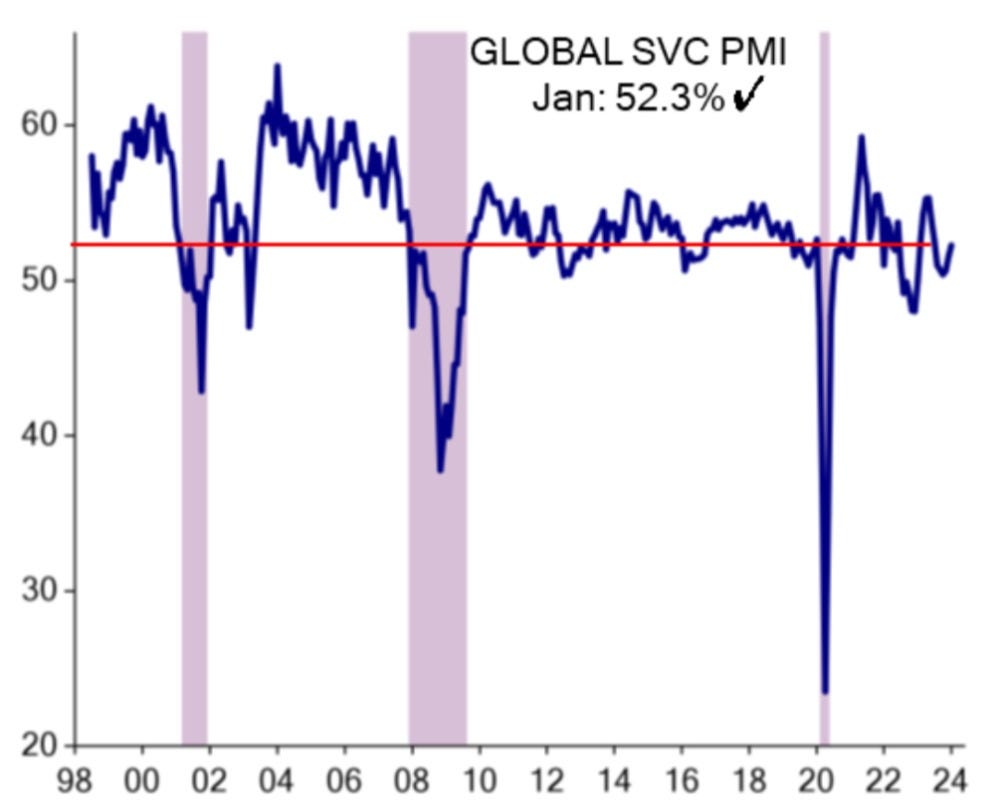

And this isn’t just a US phenomenon, have a look at the Global PMI. (graph from Ed Hyman of EvercoreISI)

Looking at last week’s survey results, most of the Services PMI were up month/month other than the China Caixin, which was down slightly but still expansionary.

Definitely a tailwind to the soft landing narrative.

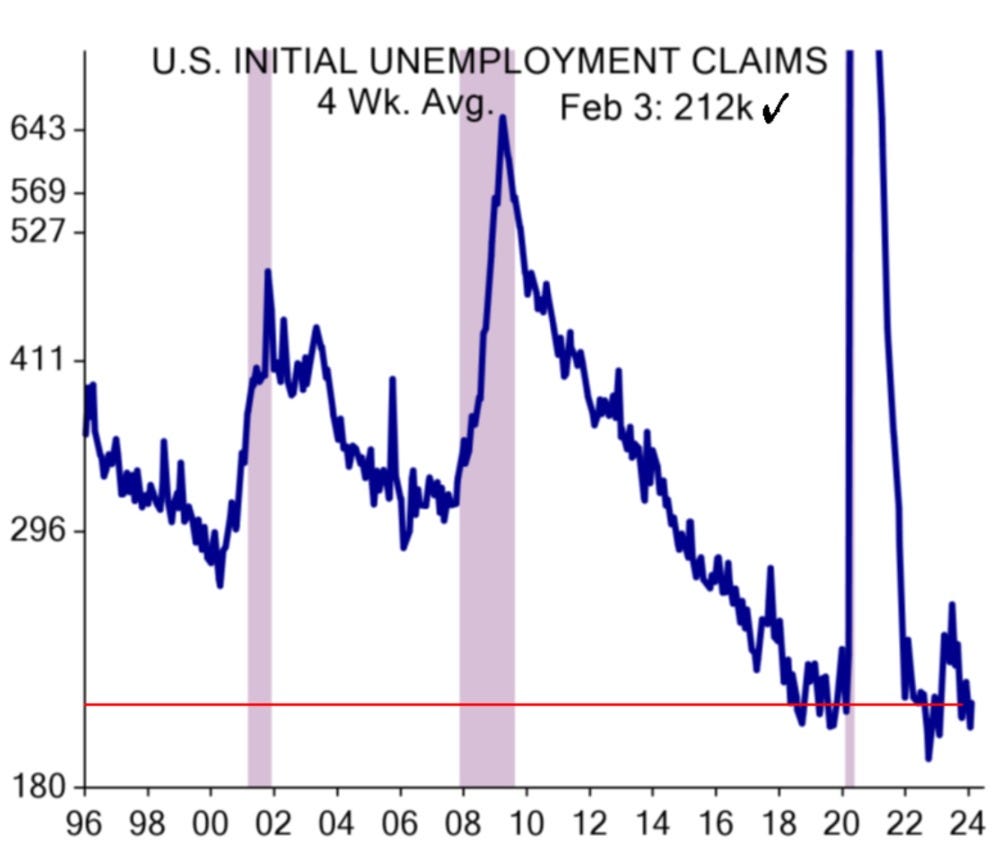

INITIAL CLAIMS - SOLID AS A ROCK

In between monthly payroll reports, initial claims is the best real time gauge of the job market and the data series continues to suggest a healthy labour market with this week’s tally of 218k, which was right in line with consensus. (graph from Ed Hyman EvercoreISI).

It is early days in February, but EvercoreISI is projecting 225k payroll gains for February.

The jobs market continues to be the anchor piece to the soft landing scenario.

Remember, the break even jobs number is approximately 100k per month.

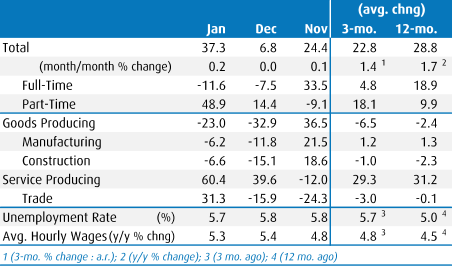

CANADA PAYROLLS - STRONGER THAN FEARED

The Canadian economy created 37k jobs in January, more than double the expected 15k result.

The biggest surprise was the decline in the unemployment rate to 5.7%, down 0.1% and the first decline in over a year.

The driver of the lower unemployment rate was an overall decline of 0.2% in the participation rate to 65.3%.

I wouldn’t call this report super high quality as part time positions (48.9k) represented over 100% of the new jobs.

Douglas Porter of BMO summed up the results rather well:

Perhaps the key takeaway from the mixed report is that there are no obvious signs of stress for the economy, at least in these results. A decent job gain, a slide in the jobless rate, and persistent 5% wage growth are hardly the stuff of an urgent call for rate cuts. The Bank of Canada is likely to view this report as further reason for patient policy stance. Douglas Porter, BMO, February 9, 2024

Here’s a handy summary of the report from BMO economics:

You can see that the 3-month average gain has decelerated by 6k jobs, or a snick under 21%. Wage growth is clearly still too hot for the BofC.

Rate cut expectations in Canada have been pushed out until June based on this report and the better GDP results reported last week.

The BofC is not quite in the position of strength of the FOMC, yet it does seem to have a bit of wiggle room regarding WHEN to start cutting, at least as it stands today.

CPI REVISIONS - ANOTHER FLY IN THE INFLATION OINTMENT DISMISSED

I decided to devote some space to discuss the annual revisions because there was lots of chatter in the financial verse about the possibility of the CPI revisions interrupting the mostly smooth decline in inflation readings we have witnessed in the US economy.

I’ll cut to the chase, the revisions were actually slightly positive to the declining inflation narrative. Over to Krishna Guha of EvercoreISI:

Post revisions a bit less of the disinflation comes from core goods, and a bit more of the disinflation comes from moderating housing services - with OER and rents down to 0.4%, the slowest pace in 2 years, in the revised December print - and from core services excluding housing (CSEH), though outright falls in goods prices in 2H2023 still makes an outsized contribution…..Post revisions, there is somewhat more grounds for optimism on OER and CSEH, and less support for concerns that last mile disinflation will be the hardest. Krishna Guha, EvercoreISI, February 9, 2024

The last line resonates with me the most as there has been a notable lag in measures of rent used in CPI and PCE calculations against other data which suggest rents have further to fall. Just so you have all the data, here is a handy table from Mr. Guha:

We get CPI next week, street is not expecting much change from the January read, we shall see. The trend is clearly down, and the revisions were simply additive to this narrative.

CME Fedwatch is suggesting a 52.5% chance of a cut at the May meeting currently, which is down from 60% a week ago.

FEDSPEAK IS PRETTY CONSISTENT THIS WEEK

The blockbuster January payrolls report notwithstanding, Fed speakers over the week were not overtly hawkish from my perspective.

The next move is a rate cut, but the strength of the economy and benign inflation allows patience. Hence the moderate pushing out of rate cut expectations as shown above.

The January 2023 booming payroll caused a more hawkish response from the Fed, as highlighted by Krishna Guha of EvercoreISI, because inflation indicators were simply not in the same place that they are today.

And of course Friday’s CPI revisions will further reinforce the continuing downward path of inflation.

This is the end of the free portion of this week’s blog, if you wish to continue reading, here’s what I will be covering:

Flows Analysis - combination of $$ flow and trading desk observations, afterall, as we all know, $$ flow is what ultimately drives stock prices.

Charts of the Week - another interesting and effective way to analyze this week’s action in the markets, and helpful in identifying ideas for follow up.

Portfolio analysis - this week I cover core positions in energy, GLP-1 and industrials.

Thanks for reading No Straight Lines Investments, best of luck this week in the market.

I post fairly regularly to LinkedIn, X (@NSLInvestments) and the Substack Chat so watch for my comments between the weekly blog. You can use the chat feature if you have any feedback or ideas you wish to discuss.