INFLATION DECLINE PAUSES, CAUSE FOR CONCERN?

INFLATION DECLINE PAUSES, CAUSE FOR CONCERN?

Hello and welcome to the latest edition of the No Straight Lines Investments blog, I am pleased you have tuned in.

The stock market has enjoyed superb performance since October due to the dual factors of better than expected growth with continued progress toward the Fed’s 2% inflation goal.

This week’s hotter CPI and PPI prints have dealt the disinflation story a setback. Juxtaposed against an SPX that was up 14 of the past 15 weeks, it is no surprise that these important releases caused a selloff in equities and an uptick in rates.

The only way to definitively conclude whether these are one offs or the beginnings of a new trend is to wait for the incoming data.

We will see the Fed’s preferred inflation measure, PCE next week, along with perhaps the most important quarterly report of this reporting season, NVDA, on Wednesday!

With that, let’s examine this week’s key macro releases.

CPI - THE OER SEEMS WONKY TO ME

Graphs from Krishna Guha, EvercoreISI

Both headline and core CPI were ahead of expectations, and in particular the core y/y reading remained at 3.9%, unchanged from December.

A resurgence in shelter inflation (see 2nd graph above) and core services inflation were major contributors to the worse than expected result.

We know that CSEH is a key measure followed by the FOMC, so the 6-month annualized rate jumping from 4.4% to 5.5% will get the Fed’s attention.

There is a plethora of data suggesting the imminent decline in OER and rent measures, we simply have not seen it in the numbers as of yet.

Ed Hyman of EvercoreISI pointed out the surge in the number of apartments being built as a harbinger of rent deflation on the horizon:

You don’t want to make TOO much of a single data release. The Fed has stressed the need to see a sustainable path to 2%, in other words, bring on more data.

No surprise, the odds of a May rate cut dropped from 61% pre-CPI to 38.6% post.

PPI - REINFLATION PART DEUX

Forgive the obvious plug, but this week’s key inflation releases prove that when it comes to investing, there simply are No Straight Lines!

PPI came in hot, but have a look at the y/y changes, and it isn’t as alarming (graph from Gregory Daco)

There is plenty of debate about seasonal factors playing a role here (the past 4 January PPI’s have been hotter than expected).

Taking the data at face value, I think the more practical exercise is examining how the PPI data will translate over to PCE, which will be released on Friday. Here’s a really helpful chart from Krishna Guha of EvercoreISI, which lays out the key components that carry over into PCE:

Guha points out that Hospital Costs and Offices of Physicians carry about a 23% weighting in PCE-CSEH.

So the takeaway is that PCE is likely to print above expectations, and we will have to wait for February data to see if January was a blip or the beginning of a new trend.

For what it’s worth, most of the big Wall Street shops are maintaining June as the first cut.

CME Fedwatch has the odds of a June cut at 53.7%, which is up from 41.9% last week. This is a surprising change given the higher inflation, to me anyway?

INITIAL CLAIMS - STILL NOT SIGNALLING ANY TURBULENCE AHEAD

As the graph from Ed Hyman EvercoreISI shows you, there is no noticeable uptrend in the claims data as of yet.

It signals a resilient labour market, which is the key support for the soft landing.

Until the labour market weakens significantly, the US economy will be in good shape.

EMPIRE/PHILLY FED - MANUFACTURING LOOKS BETTER

As you folks know, I have been thinking that the Manufacturing economy is set for a rebound.

This week’s Philly Fed and Empire Manufacturing surveys showed a solid bounce back, as captured in this handy blended graph from Ed Hyman

Here’s what Goldman Sachs Joseph Briggs/Devesh Kodnani had to say about manufacturing in a recent report:

We believe that manufacturing activity has troughed and should improve on the back of resilient global growth and the arrival of central bank rate cuts in 2024. Indeed, our estimates suggest that each 100 bps in rate cuts (or an equivalent easing in financial conditions) leads to a 1-1.5 point pickup in manufacturing PMI’s Devesh Kodnani/Joseph Briggs, Goldman Sachs, February 13, 2024

To be balanced here, the report also suggests that elevated inventory levels and still above trend good spending will ensure that the manufacturing part of the economy doesn’t overheat.

All that being said, it does look like manufacturing has bottomed and is heading back toward expansion in 2024.

I have been playing this theme through copper and steel. I am continuing my work on the transports/industrials as a whole, I haven’t made any decisions yet.

RETAIL SALES - WEATHER PUT A CHILL ON THE NUMBERS?

For the first time in 9 months, control group retail sales declined. I chose this graph (from Liz Ann Sonders) as this is the data that feeds through to GDP calculations.

Noteable that many of the bears were prominent on X post the weaker retail sales release, going so far as to say that the combination of higher inflation + weak retail sales equated to stagflation. C’mon man!

We can only say with certainty that the data is an aberration after seeing a few more months, that’s just the way it is.

Is it possible that weather had an impact? It absolutely is, let’s see what February looks like.

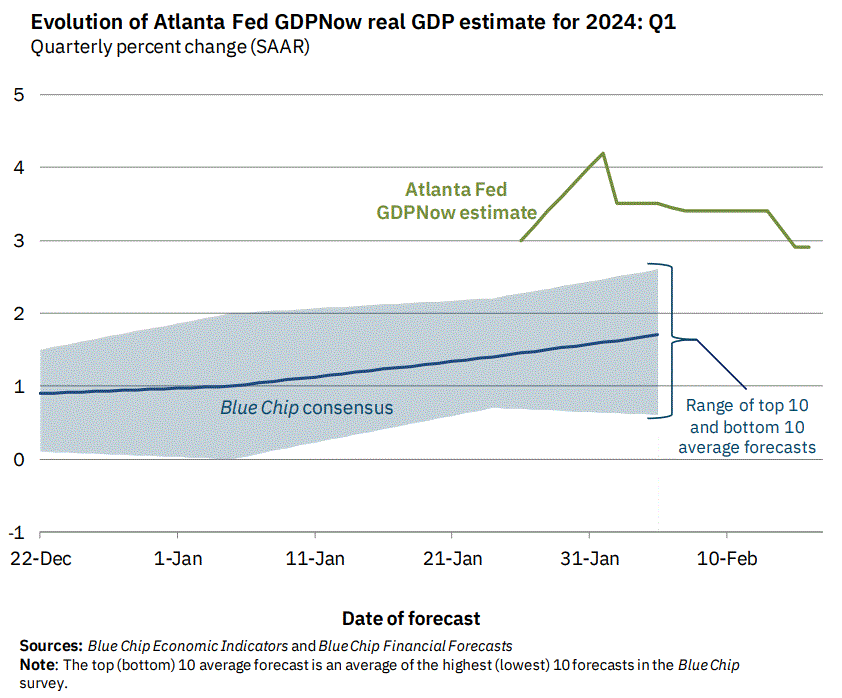

GDP NOW REVISED LOWER, BUT STILL A HEALTHY PROJECTION

With the weaker retail sales and housing numbers this week, GDP now was revised lower to 2.9%. GDPNow is beginning to converge with the consensus.

The biggest component by far of the Q1 estimate is consumer spending at 1.82% (of the total 2.9%).

The health of the jobs market is the key determinant of consumer spending.

FEDSPEAK - NON VOTER GOOLSBEE AND FORMER ST LOUIS FED PRESIDENT BULLARD DOVISH, BOSTIC NOT SO MUCH

Post the hot CPI, Austan Goolsbee, President of the Chicago Fed, suggested that it would be a mistake to wait for inflation to hit 2% prior to cutting rates.

If you see inflation go up a little bit, that doesn’t mean we aren’t on target to get to 2%. We can still be on that path even if we have some increases and some ups and downs. Austan Goolsbee, February 14, 2024

Goolsbee made reference to the FOMC’s preferred PCE measure, which checked in at 2.9% in December.

As I highlighted above, based on the PPI/CPI inputs, core PCE is projected to register 0.4%, the highest reading in a year, and would hold the y/y number at 2.9%.

Former governor Bullard, was notably dovish in comments at the NABE conference:

I’m worried you’re going to get into Q3 and the policy rate is going to be too high….You don’t have to say you’re going to do six moves. You would say, ‘We’re making one move based on the data that we have in hand, and we’re not guaranteeing anything more.’ James Bullard, February 16, 2024

Obviously Bullard has no sway with the FOMC, however, he was on the hawkish side of the Fed so his change in opinion is worthy of mention.

Raphael Bostic, President of the Atlanta Fed had somewhat less comforting words:

The evidence from our data, our surveys, and our outreach says that victory is not clearly in hand, and leaves me not yet comfortable that inflation is inexorably declining to our 2% objective. That may be true for some time , even if the January CPI turns out to be an aberration. Raphael Bostic, February 15, 2024

Everyone clear now?!

I think the point is that the hot inflation prints from this week will stoke some uncertainty around the path to 2% until we get more data.

This is the end of this week’s free post.

If you read on, here’s what I have in store:

Flows - weekly $$ flow stats and trading desk colour, it is crucial to understand where the $$ are going, it is ultimately what drives stock prices.

Q4 Earnings Summary - what are the revisions for Q4 adding up to and what sorts of margins and revenue growth assumptions are driving estimates for 2024 on the whole.

Charts of the Week - some really interesting highlights this week, you might find your next idea here.

Portfolio Stock Write Ups - I take profits in one of my names that has been on a tear, introduce a new idea (haven’t purchased yet), and three other updates that I believe you should read about.

As always, I would love to hear any feedback or suggestions, this is meant to be a two way street.

Thanks for reading, you can follow me on X (@NSLInvestments), or on LinkedIn, or check out the Chat feature on Substack, I generally post during the week on things of interest.

Good luck this week!