MARKET DIRECTION DISTINCTLY DATA DETERMINED

MARKET DIRECTION DISTINCTLY DATA DETERMINED

Hello and welcome back to the No Straight Lines Investments blog, thanks very much for joining me.

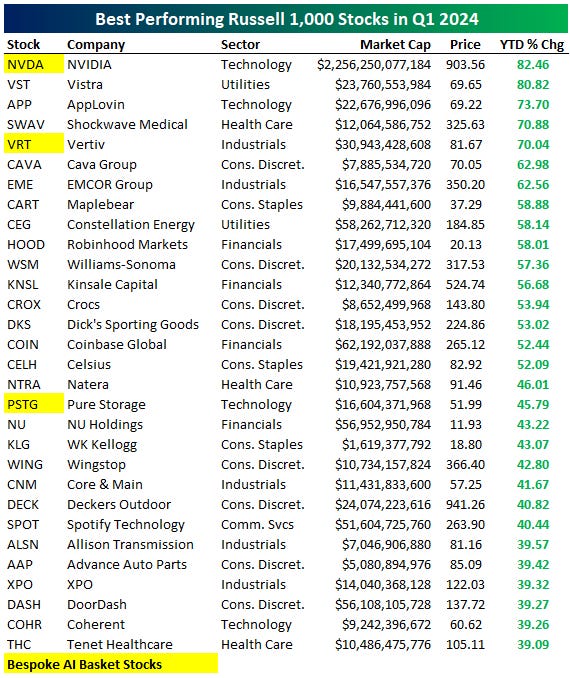

Q1 is in the rearview mirror and whilst we had some stocks perform as expected, think AI winners, there were definitely some surprises (aren’t there always?). Have a look at this chart from Bespoke:

I would point out that VST and CEG are part of the AI Power theme.

As a nod to how humbling investing can be, I owned both VRT and DKS, and sold both, as it turns out, with plenty of gas left in the tank!

I will be detailing some of the surprise outperformers from Q1 in my Charts of the Week, and provide my two cents on where we go from here with these assets/stocks.

This past week was the first week since JPow and the FOMC took a more dovish turn. What that really means is that we are more acutely occupied with parsing incoming data in the context of sustained progress toward 2% inflation.

Of course this has always been the case.

However, if we are to believe the FED dot plots and buy into 3 rate cuts this year, there is a much larger onus on the next few months inflation data adhering to the prescribed downward path.

And my comments presume that the soft landing continues to be supported by the data, which may be an overreach, we shall see!

A few quick observations about this week:

The 10-year treasury yield was unchanged at 4.20%. Hmmmm.

In a week that saw underperformance of some of the leaders (NVDA/MSFT/META), it was encouraging to see 414 SPX members positive on the week (thank you Joe Anastasio GS). That is called positive breadth folks.

On to the week that was.

PCE AND JPOW - FEBRUARY DATA A MODEST REPRIEVE

Graph from Krishna Guha, EvercoreISI

Core PCE came in at 0.26%, slightly below expectations of 0.3%. The 6-month annualized rate of 2.9%, was up 3 ticks from January, and is considered by the FED as the best frequency to assess inflationary pressures. Stay tuned.

February once again exhibited core goods inflation of 0.3% m/m. I am pointing this out because we need to see continued services deflation to offset the normalization in goods prices.

On that front, CSEH came in at 0.18%, but 6-month rates remain sticky at 3.8%.

Finally, housing clocked in at 0.4%, a 1 tick deceleration from January and a welcome read. Most analysts expect OER and housing to continue along the path of disinflation based on new market rent data.

As with all inflation statistics, there is a low tolerance for upward misses on anything related to housing.

In an unusual circumstance, JPow was speaking at the SF Fed post the release of the PCE data.

Krishna Guha of EvercoreISI summarized his speech thusly:

In comments in a fireside chat hosted by the SF Fed, the Fed chair said that it was good to see the release coming in line with internal Fed estimates post CPI and PPI. He characterized January as “very hot” and February “definitely more along the lines of what we want to see” though he noted that it was still not as low as many of the good readings in late 2023……..

Powell confirmed the base case is that “we expect inflation to come down on a sometimes bumpy path”. And he said that the Fed is telling us what it would do if this base case expectation is supported by the incoming data-which we would read as a reference to the SEP median three cuts this year with the implication that the first cut would come in June. Krishna Guha, EvercoreISI, March 29, 2024

I guess the big question is whether the market NEEDS the Fed to start cutting rates in June in order to continue with it’s outstanding performance?

According to CME Fedwatch, there is a 61% chance of a 25 bps cut in June, which is down from 66.7% a week ago.

The market has gone up even as rate cuts have been taken out of the market (we began the year pricing in 6 cuts) and with hotter inflation prints.

My playbook presumes we see inflation continue to decline, but much like central banks globally, if the narrative changes I will adjust accordingly.

CONSUMER SPENDING - POTENTIAL SIGNS OF SLOWING

Real personal consumption spending came in stronger at 0.4% against consensus of 0.1%.

Meanwhile, real disposable income declined 0.1%, and the savings rate also dropped to 3.6%.

Graph from Krishna Guha, EvercoreISI

The implication is that consumers drew down savings in order to spend $$.

As I have said many times, it doesn’t pay to bet against the US consumer, but this is certainly worth watching.

This report is supportive of an increasingly strong looking Q1 GDP print. GDPNow was revised up to 2.3% on Friday.

INITIAL CLAIMS - BORING IS GOOD

Initial jobless claims are exhibiting much less volatility, at least over the past month. They remain the best real time indicator around the health of the labour market. Claims for the past week were 210k against 213k consensus.

Graph from Stan Shipley, EvercoreISI.

According to Mr. Shipley, claims for March are consistent with 225k job gains. We get the payroll report on Friday, which remains the single most important monthly data release.

CANADA GDP - HEALTHY PRINT, NO RECESSION IN SIGHT

Instead of a negative revision to January’s flash GDP estimate of 0.4%, we got a 0.6% print.

Not only that, the preliminary February estimate is almost equally strong at 0.4%.

To put these numbers in perspective, according to BMO’s Douglas Porter, if February’s flash estimate holds and March is 0%, Q1 growth would be 3.5% annualized.

The BofC’s MPR(Monetary Policy Report) had predicted 0.5% for Q1 and 0.8% for all of 2024.

Mr. Porter revised his full year GDP estimate to 1.2% (from 1%) based on the stronger report.

It is important to note that in 2023, the first few months were similarly strong before petering out for the rest of the year. So there could be some statistical noise showing up at the beginning of the year.

For now, the strength of the report (recognizing much of it was driven by government spending) suggest slightly less urgency for the BofC to cut rates.

For those chiding the high proportion of government as a component of GDP, remember, the US has run budget deficits averaging 9% of GDP for the past 4 years, and much of the strength in manufacturing is a result of heavy subsidies to promote onshoring. Not meant to be critical, quite the opposite, I think it was bold policy. But it is government derived demand ultimately.

Odds of a June rate cut sit slightly below 70%, which is only a very moderate downtick from futures pricing prior to the GDP release.

All else being equal, far better for the BofC to be cutting from a position of strength, particularly as it pertains to equities.

Handy chart with all the key data from BMO’s Porter.

U of MICHIGAN YEAR AHEAD INFLATION EXPECTATIONS - NO ENTRENCHED VIEWS

This is a graph at which the FOMC will enjoy gazing.

Year ahead inflation expectations dropped to 2.9% in the latest UofMich consumer survey.

You can see that the blue line has been quite volatile but appears to be slowly heading toward that magical 2.5% level. Interesting that it never reached 2% in the history of the chart.

Regardless, this is a supportive inflation data point for this week.

That’s it for key economic releases this week.

If you want to continue reading, you can sign up for $20/month. Here’s what’s in store:

Flow Specifics - if you want to understand why stocks are moving, a great place to start is $$ flows. Price action is, afterall, about demand and supply.

Charts of the Week - always an quick way to understand the week that was. This week is slightly different as I am going to feature the best sectors in Q1 along with some weekly picks.

Portfolio Stocks - I will discuss my lone small cap energy stock and will delve further into the electricity boom driven by onshoring, the push to electrify everything and, of course, AI data centres. The average unweighted return is 29.4% on the stocks I have written up since I began the blog. Maybe you uncover your next idea to investigate?

Life Hacks - stay tuned!

If this is it for you, thanks for reading, I appreciate your time.

Good luck in the markets this week!

I tend to post comments throughout the week, you can follow me on X (@NSLInvestments), or on LinkedIn, or through the chat feature on Substack.

Please reach out if you have any feedback or want to debate anything I have discussed.