SETTING THE TABLE FOR 2024

Hello and welcome back to No Straight Lines Investments blog, Happy New Year to you all and thanks so much for joining me here!

Let’s state the obvious, 2023 did not go as planned!

This post is going to be slightly different than the usual, as I want to provide some details around my base case and then get into the names that I expect to be solid money makers for me over the next year!

ECONOMIST OF THE YEAR

Hopefully there is a benefit to close to 30 years of investing. At the very least, it is important to recognize when an individual prognosticator has a hot hand.

On the economics front, over the past year, that person has been Jan Hatzius of Goldman Sachs.

Much like Tom Lee of Fundstrat has called the equity markets remarkably well, Mr. Hatzius remained more sanguine on the global economy when everyone was convinced of the imminent recession. His current recession probability in the US is 15%, for what it’s worth. The steady state assumption is that there is always a 25% probability of a recession (according to Hatzius) so this assigned percentage is indeed low.

As a starting point, what does Mr. Hatzius forecast for US GDP growth in 2024?

2.3% is the number.

For a quick compare, here are the tally’s for some of the other big shops:

MS - 1.9%

JPM - 0.7%

C - 2.2%

BofA - 1.2%

Street Average - 1.66%

Clearly Goldman is the most bullish.

The real question is WHY?

Have a read of the direct quote below as it summarizes rather well:

The big surprises of 2023 were the sharp outperformance of global growth - which exceeded expectations by 1% - and the rapid normalization of inflation in the 2H of the year. The upside growth surprise reflected a fading drag from monetary policy tightening (as the lag from changes in financial conditions to growth is much shorter than commonly appreciated), as well as a recovery in income growth that kept consumer spending growth solid. Jan Hatzius, December 29, 2023

Mr. Hatzius is far too modest to call out any of his colleagues but the bolded line is the whole reason why he was not as bearish.

If you read the current bear thesis, it can be summarized quite simply: the tightened financial conditions work with a lag and we haven’t yet seen the full impact of those tighter financial measures on the economy.

This is why the inverted yield curve or the many months of consecutive declines in the LEI’s or the decline in M2 are viewed as harbingers of a much slower economy i.e. recession.

Obviously it is too early to declare victory, although I would argue the bearish folks just cost investors who followed their advice some significant returns over the past 12 months.

However

The next chart is a superb graphical representation of precisely what Mr. Hatzius is referring to in the bolded text above:

The most interesting aspect of the graph is that Q4 (which we just exited) will be the last Q where FCI is a drag on the economy.

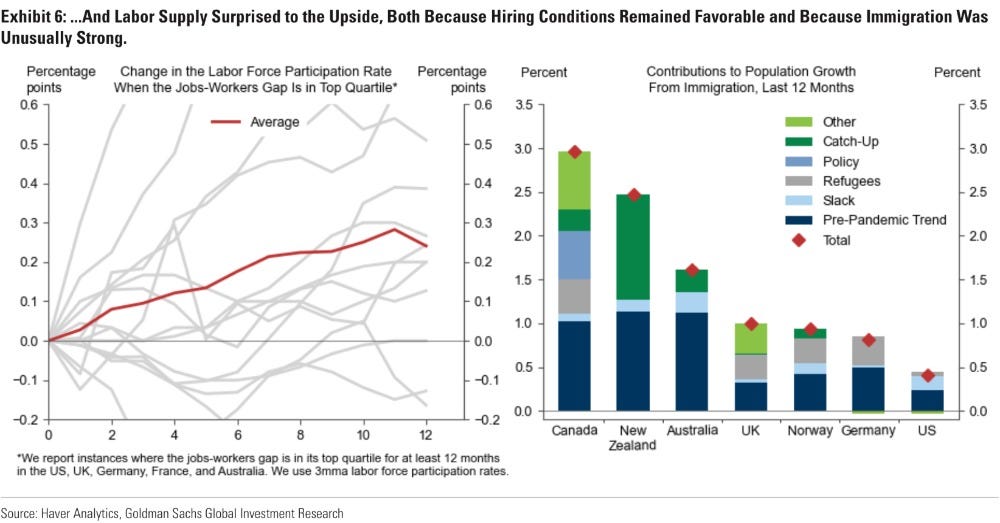

The progress on inflation despite firm growth underscored the unique nature of this cycle. Labor market balancing progressed smoothly as excess job openings unwound - despite unemployment rates remaining low - while labour supply beat expectations (both due to favorable hiring prospects and an immigration rebound). Combined with improving global supply conditions (which lowered core goods and headline inflation), this softened the upward pressure on wage growth, which should settle at a sustainable level in the year ahead. Jan Hatzius, December 29, 2023

It is always dangerous to say it is different this time. Especially when you say it without actually saying it?!

Wage inflation has been somewhat stickier than anticipated (especially in Canada), but the decline in job openings, should, all else being equal, also start to lessen the upward pressure on wages (along with goods deflation as referenced by Mr. Hatzius).

I am highlighting wages as it is truly the only aspect of the jobs picture that wasn’t Goldilocks.

For some perspective on the impact of immigration, have a gander at the following chart, pretty interesting:

It is not hard to see how the higher levels of immigration without productivity improvements, have led to 6 consecutive quarters of GDP per Capita declines in Canada. Canadian businesses need to reinvest in capital equipment to start to move those productivity numbers the other way.

Weekly initial claims are the best real time gauge of the job market, and this past week’s reading at 218k is still not registering any alarm bells with the labour market.

We get December payrolls on Friday, and there is likely a bit of upside bias to the 168k jobs estimate.

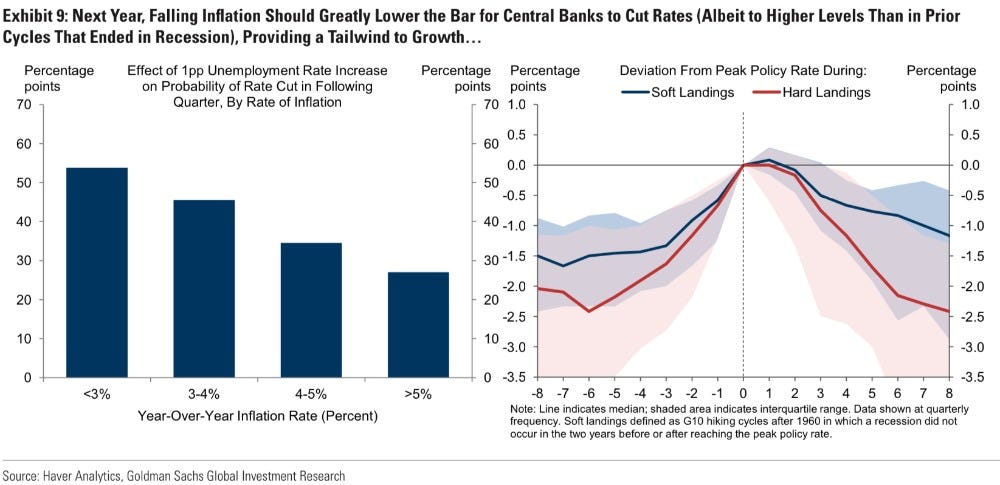

As inflation nears the finish line, the bar to cut rates has fallen, and central banks should begin to normalize next year. Jan Hatzius, December 29, 2023

I don’t think anyone would argue that rate cuts will be a tailwind to equities.

The bigger question is whether the rate cuts are happening during a growth slowdown or an outright recession?

I thought this chart was really interesting:

Worth noting that the y/y inflation rate should be below 3%, and so a 0.1% increase in the U rate would create >50% odds of a rate cut.

There are concerns around the fact that the market may have gotten ahead of itself in terms of number of rate cuts priced in next year (currently 6).

Should that prove to be too optimistic, it is likely due to better than anticipated growth in the economy, which is NOT a bearish outcome.

CONCLUSION

Some of the folks at Goldman have called the Hatzius forecast the “Everything is Awesome” forecast, in reference to the hilarious song from the Lego Movie.

I understand why it is somewhat challenging to accept that the soft landing is achievable, particularly given all the lagging indicators I referenced above.

I am inclined to put my chips in the Jan Hatzius camp. He has been way more right than wrong, and none of his assumptions appear to be aggressive.

The starting point for all of this is the jobs picture. As it stands right now, the labour market is exhibiting remarkable resilience and strength. So long as that continues, there is no reason to believe we are heading for a recession.

I believe that the string of benign inflation readings will allow the Fed (and the BofC) to cut rates sooner and more rapidly than investors would have imagined even just a few short months ago.

Remember “higher for longer” at the beginning of October?

I still maintain that investor positioning is not aggressive. The best evidence is the amount of sidelined cash. I am not anticipating any great amount of this stash to come into the equity market over the next year. If that happens, it will represent an upside scenario.

Here ends the free portion of the blog. If you wish to continue reading (and I would strongly encourage you to do so), here’s what I will cover:

Charts of the week - for this week I will be going over many of the stocks in my current portfolio and expectations for the next year.

Bonus Charts - a selection of several pictorials/graphs that highlight how investors were positioned at the beginning of 2023 and also how current performance trends may auger for 2024. Quite eye opening.

If this is where your reading ends, thanks very much for joining me. The best of luck for this first week of 2024!