STRENGTH IN NVDA STOKES BREADTH IN THE MARKET

STRENGTH IN NVDA STOKES BREADTH IN THE MARKET

Hello and welcome back to the No Straight Lines Investments blog, thank you for reading, whether you are a regular or a first timer!

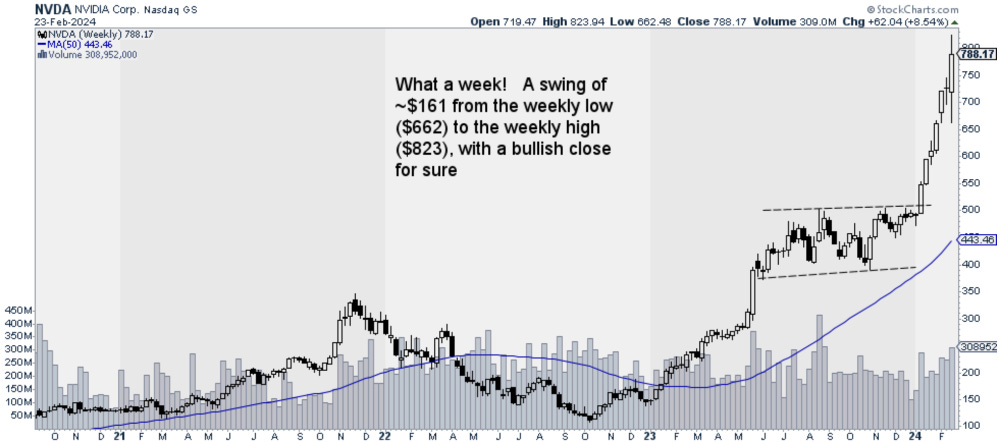

The market was on pause until NVDA numbers were released on Wednesday after the close, and the results along with forward guidance were nothing short of magnificent.

A few key takeaways from my perspective:

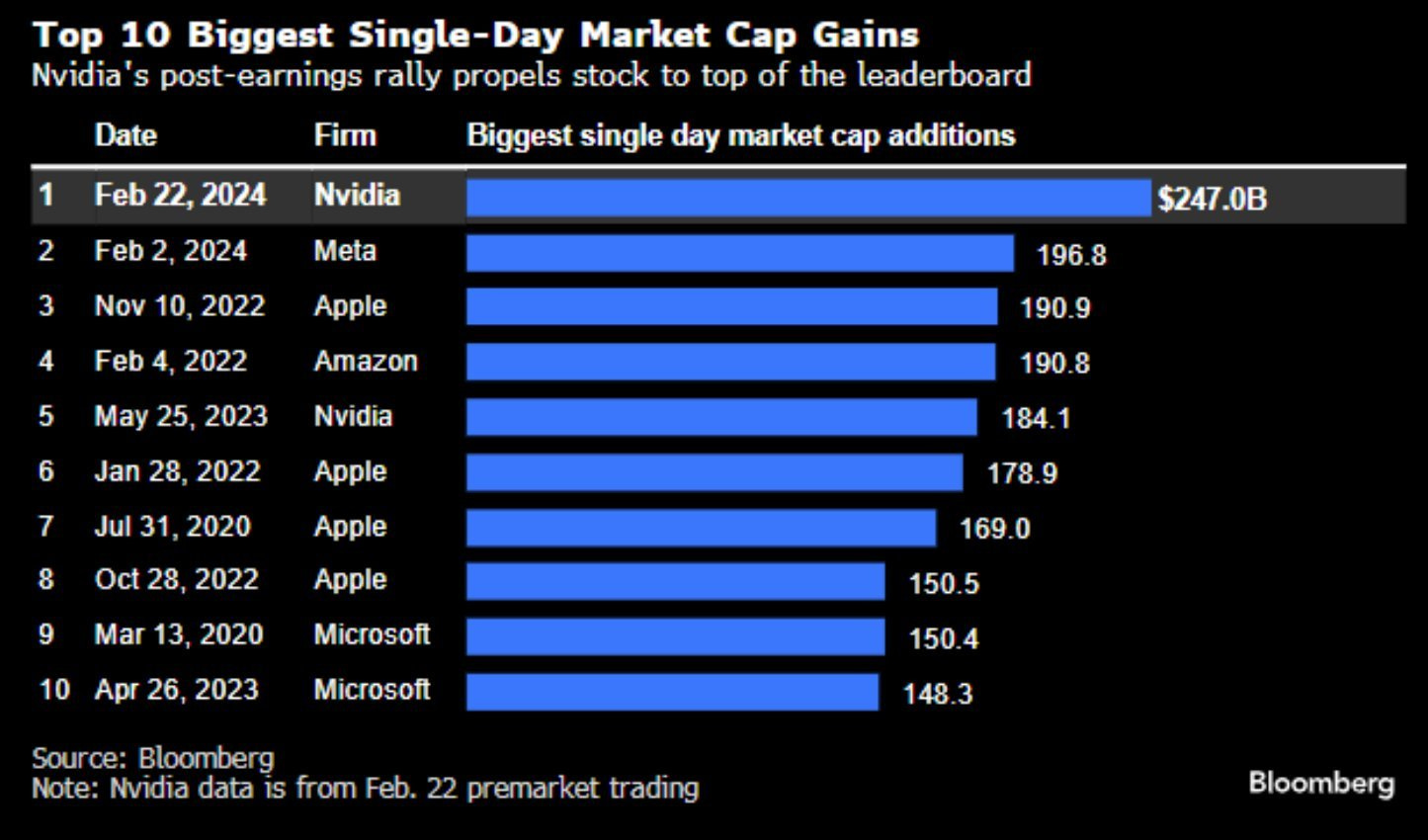

The one day gain in NVDA market cap of $247B broke the less than a month old record of $197B held by META for biggest one day increase. Amazing! Here’s a list of the top 10 in case you are curious:

The rise of NVDA led to more hand wringing about the concentration of performance in the S&P and NDX (22% of the S&P advance on the week was driven by NVDA, for example). Beneath the surface there is increasing breadth (390+ SPX stocks were up on the week) and the strength of the AI-fueled earnings provides cushion at the index earnings level for other sectors to potentially fill in, if, and I know this is heresy at this point, the market is unwilling to pay a higher multiple for the AI mega caps (currently 29x based on consensus).

For a perspective on the earnings lift, a really neat tidbit from Tony Pasquariello of GS: the Mag7 grew sales by 15% and earnings by 60% in Q4. This on the back of margin expansion of over 6%. So the Mag7 are doing more than there fair share!

Outside of NVDA, manufacturing green shoots continue, members of the FOMC were hawkish about the path of rate hikes and Canada CPI provided a downside surprise.

I will analyze the key macro events in order of importance. Without further adieu.

FEDSPEAK - WITH TOO MANY SPEAKERS TO MENTION, TONE WAS UNIFORMLY HAWKISH

Don’t take my word for it, as I mentioned to you folks at the outset of 2024, I am quite content to piggyback on the thinking of Jan Hatzius of GS. He has been the most right about the economy and rates.

This week he pushed out his first cut expectation until June and now expects 4 cuts in total (5 previously). The change in thinking is due to January Fed minutes and Fedspeak this week. Here are the key lines:

The preference to wait somewhat longer appears to reflect two changes in Fed thinking. First, as strong activity data have piled up, Fed officials have become less concerned about the risk of keeping the funds rate too high for too long…..Second, in contrast to the earlier emphasis on 6-month annualized rate of core PCE inflation and Chair Powell’s indication that cuts should come “well before” inflation reaches 2%, Fed officials now appear to be taking a more cautious approach of wanting more definitive evidence that inflation will approach 2% before cutting, in part because some worry that the stronger performance of the economy could inhibit further progress in reducing inflation. Jan Hatzius, GS, February 22, 2024

The end result is that markets are now pricing in roughly 80 bps of easing by the Fed this year, which more or less lines up with FOMC baseline of 3 cuts in 2024.

Governor Waller’s comments seemed to be the most influential, and the fact that he ended his speech with the question “Why rush?” tells you everything you need to know.

Key points made by Waller, which were more or less mimicked by Kashkari/Bowman/Bostic/Jefferson:

Needs to see at least a few more months of inflation data before cutting. This comment took a May cut off the table.

He continues to expect cuts later this year, but sees risks to inflation on the upside due to the strength in economic data.

The decision to be patient with cuts is simple given the recent data.

CME Fedwatch pegs the odds of a cut in June at 52%, which is down from 55.3% one week ago.

Notable that the 10-year was down 4 bps on the week to 4.26%. Interesting.

MANUFACTURING PMI - ANOTHER EXPANSIONARY READING

The S&P Flash Manufacturing PMI registered 51.7, which signals the fastest growth since September of 2022.

New Orders grew were up the most since May of 2022, along with Export orders growing after 2 months of decline.

Finally, Factory output expanded for the first time in 3 months, and reached it’s highest level since April of last year.

There are a lot of positive signals here, let’s see if the ISM confirms the trend this coming Friday, current consensus expects a reading of 47.8.

In the meantime, Michael Hartnett of BofA put together some interesting charts tracking Global Manufacturing ISM against indexes and sectors:

The two that I wanted to highlight are as follows:

It is clear that materials stocks do not reflect much optimism of a manufacturing (or overall economic) expansion at this point. I am sticking with my copper positions as the risk/reward skews rather favourably, in my view.

Some of the industrials (like LTL Truckers) are certainly pricing in a fairly robust manufacturing recovery. That is not the case with steel, or at least not STLC.

The flash S&P reading for US Manufacturing is bullish for the US economy.

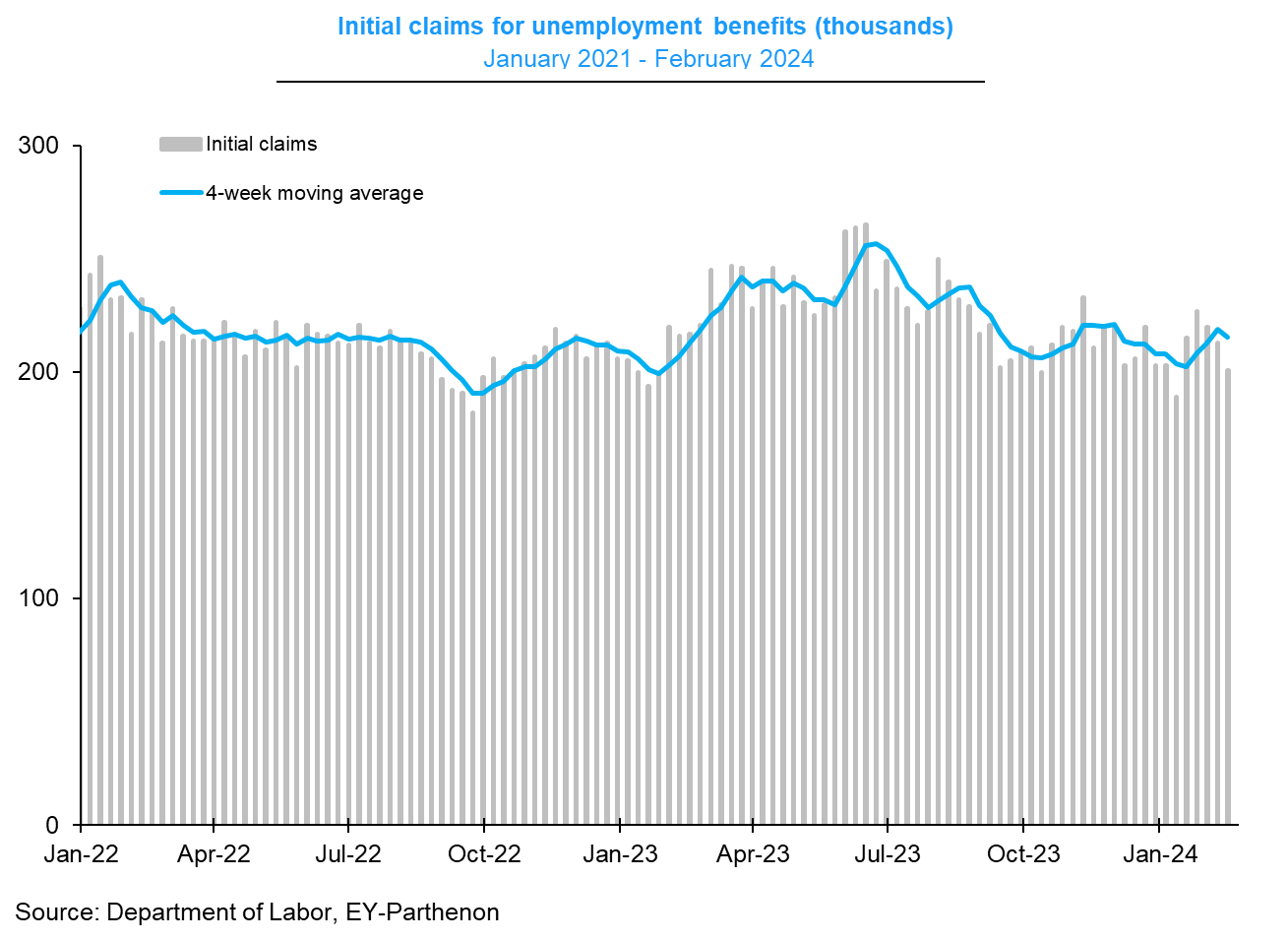

INITIAL CLAIMS - CRUISING

Chart from Gregory Daco

As you can see, there was a drop in initial claims this week to 201k, which was handily below the consensus expectation of 216k.

There is no payrolls report next Friday, therefore, initial claims will remain the best real time indicator of job market health.

At current levels, the labour market is exhibiting no signs of stress, which means the anchor of the soft landing remains rock solid.

CANADA CPI - MR. MACKLEM YOU ARE RUNNIN OUT OF EXCUSES

You see the dark blue line is below that magical 3% level (actual reading for January was 2.9%)? This is only the 2nd time CPI has dipped below 3% since March of 2021.

So we are within the target range of 2% to 3% inflation.

As for the measures closely tracked by the BofC, here’s how they look:

Trim - 3.4% annualized, down from 3.7% in December

Median - 3.3% annualized, down from 3.5% in December

Check.

The biggest driver of Canadian inflation remains……mortgage interest cost.

In fact, if you exclude mortgage interest, inflation is bang on 2%. (thank you Douglas Porter)

Here’s a handy table of all the critical numbers from BMO’s Mr. Porter:

Obviously the BofC is going to want to see a continuation of the disinflation trend, but the January numbers suggest that April is still on the table for a rate cut, at least from this blogger’s seat.

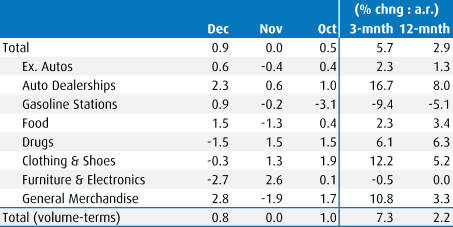

CANADA RETAIL SALES - STRONG FINISH TO 2023, SLOW START TO 2024

Retail sales growth of 0.9% for December, was modestly ahead of the expected 0.8% increase.

This was the strongest growth showing since last April.

The November estimate was nudged up to flat from the previous -0.2% reading.

Overall, Q4 retails sales are up 1%, which is the second consecutive quarter of retail sales growth in Canada.

Unfortunately, the advance estimate for January was -0.4%, which would be the weakest number in 9 months.

So where does this leave the Canadian economy?

It looks like Q4 GDP will be ok, perhaps slightly stronger than StatsCans 1.2% estimate, which will be released this week.

The BofC expects 0% GDP growth over the next 2 quarters, so the early retail sales estimate for January seems to dovetail with this forecast.

Here is a data table for your reference from BMO’s Shelly Kaushik:

The January retail sales reading probably slightly weighs in favour of an earlier cut by the BofC, we will await further data to confirm.

This is the end of the free portion of the blog. If you would like to continue reading, and I think you should, here’s what’s in store:

Flow Analysis - where are the $$ being allocated, and what is the client activity on trading desks? Some surprising insights this week that run counter to the narrative.

Charts of the Week - an efficient method to capture the zeitgeist of the week in equities, and perhaps find your next great idea.

Portfolio Company Comments - the average unweighted return for the stocks I have analyzed in the blog is 21.3% since inception. This week I provide comments on 4 of my names, 3 in materials and 1 in consumer discretionary.

Some Useful Life Hacks - health tips, book and streaming reco’s along with random music playlists, how could you resist?

If you are finished here, thanks for reading, and if you have any questions/feedback, feel free to reach out, I am always interested in hearing from readers.

Best of luck this week!

If you follow me on X (@NSLInvestments)/LinkedIn or use the Substack chat, I make comments throughout the week on things that I think are worthy of discussion.